Diesel Downhill

Diesel fuel is the lifeblood of this oh-so high-tech civilization of ours. Without it there is no mining, no transportation, no agriculture. At least not at any meaningful scale. Contrary to all the happy talk of electrification reducing oil demand, there is no replacement for this incredibly energy dense and versatile fuel. The problem is: we seem to be unable to make enough diesel to satisfy demand, and the prospect of running on empty one day starts to look very much real. Are we at the end of the world, witnessing the onset of a “truckpocalypse” then? Well, let’s not get ahead of ourselves just yet.

If you thought that the economy has been growing and that the world has been getting richer in the past two decades, I have to disappoint you. It has not. Perhaps it comes as no surprise that the Gross Domestic Product (GDP) — used by those in power to reassure the masses that everything is just fine — is an entirely false metric. As opposed to evaluating real economic activity, all GDP measures is the amount of financial transactions taking place. Sure enough, with the inclusion of finance, insurance and real estate (the FIRE sector) combined with an ever increasing debt bubble, governments printing money and ballooning financial shenanigans (mortgage backed securities, stock markets, crypto currencies, NFT-s and the like) there is a hell-of-a-lot of money changing hands these days… Too bad, though, that these purely fictional activities do not add a scintilla of value to the economy. In fact, quite to the contrary: they act as a detractor. As Tim Morgan from Surplus Energy Economics explains:

The expansion in credit creates an increase in transactions in a way that artificially inflates reported GDP. If we back out this credit effect, we can calculate underlying or ‘clean’ economic output […]. Globally, this increased by only 36%, rather than 103%, between 2002 and 2022. Within reported “growth” of $83tn between those years, fully $56tn, or 67% of the total, was a purely cosmetic effect of credit expansion.

In case you were wondering: world population was 6.2 billion in 2002, and reached 8 billion in 2022 (a 29% growth). Thus, on average ‘clean’ GDP per capita grew only 5.4% over these twenty years: that is a quarter of a percent a year. Think about that for a moment. Now, if you consider how that increase in financial activity (GDP) was distributed in the world, or how inequality grew even within the wealthiest of nations during these years — not to mention how under-reported real inflation is — it is not hard to see how the average world citizen actually got poorer, and not richer.

Thank you for reading The Honest Sorcerer. If you like what you read here please subscribe for free. If you can afford it, you might want to consider a paid subscription, or leaving a tip. Every donation counts, no matter how small. Thank you in advance!

As I, and many others keep telling: Energy is the Economy. Money is not the economy. Money is a claim on products made by others, and since every value added activity requires energy, ultimately money is a claim on energy itself. If you want to use an analogy from biology: energy equates to glucose in your blood, while money is the insulin (and other hormones) telling where that energy transported as sugar should go. And while you can fly really high on a rush of hormones, you will still starve to death if you don’t eat. Similarly, without energy the economy too would come to a screeching halt. As simple as that.

Now, the question poses itself: is there any better way to report real economic activity, other than using fictional metrics based on prices and money? Yes, and as you might have already guessed, it is diesel consumption.

Since diesel fuel is essential in successfully performing almost all (real) economic activity these days from mining to agriculture and transportation, its actual consumption is a much better metric of growth, than any other financial number you can come up with. As the output of products grow at a factory, for example, so does the number of trucks filled with raw materials arriving to (and leaving from) the plant increase. If we expect the average world citizen to live “better” (purely in capitalist terms), we must assume that he or she will eat, use and dispose of more and more products year after year — all carried around on trucks — and thus drive up the demand for diesel.

But, but, but…! What about efficiency gains?! Surely you jest. Diesel engines are in use for more than a century now. There is really not a lot of practical efficiency gains left to be made here: the last great advancements in fuel economy were achieved in the 70’s and 80’s, that is half a century ago. Between 2002 and 2016 not an iota of improvement was made in actual on the road fuel consumption of heavy duty trucks. This is especially true since the diesel-scandal in 2016, after which vehicle manufacturers decided to hop on the electrification bandwagon en masse, and stopped all investments in this centuries old technology. (The irony, that electrification still hopelessly depends on heavy machinery operating on diesel, was somehow lost on them.)

{kind=link}

Now, with that out of the picture, let’s see how diesel consumption actually fared on a per capita basis globally. (Remember, every newcomer to this capitalist utopia needs a house, clothes and food at a minimum, and a range of consumer goods at best to live a “happy” life — all mined, harvested and delivered to them via this fuel.) According to the Statistical Review of World Energy global diesel/gasoil consumption grew from 26.1 million barrels a day in 2012 to 28.2 million. Even in absolute terms this is still just an 8% growth over a decade — a rather modest increase, if you ask me. On a per capita basis though, this translates to an actual decrease of 4.5% during the same period (1.34 barrels per head annually in 2012, versus 1.28 in 2022) — indicating an actual fall in prosperity. Well, it seems, all that increase in financial activity measured by GDP has indeed failed to materialize in real economic growth for the average human.

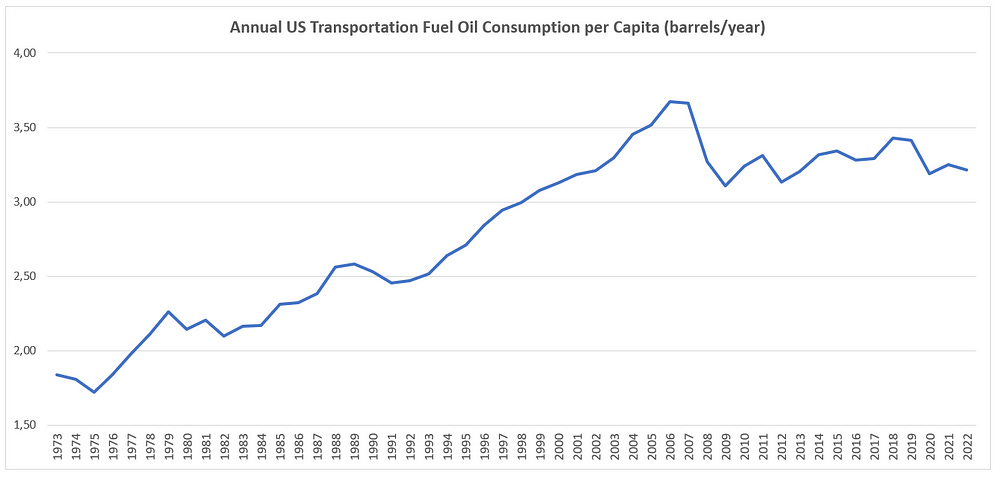

This trend is even more clearly visible in the Western world, where more detailed and closely tracked data is available. According to the EIA distillate fuel oil consumption by the transportation sector peaked in 2007. After growing for more than 30 years it has crashed in the wake of the 2008/2009 financial crisis and has failed to recover ever since, despite a 12% growth in US population (theoretically demanding more food, products and services). Consumption per capita was thus stagnating ever since the great financial crisis, and has been clearly trending downwards since 2019 — with no end in sight. The average citizen, as a result, got poorer, more exploited and less resilient, while the well-to-do, well, became even more well-to-do — but only on paper. Their actual consumption did not appear to grow in line with their wealth. Now, having all this in mind, and as a cue for the near future, read the following headlines:

Truckers Grapple With Rising Diesel Costs And High-Interest Rates

“Despite some signs of demand improvement, including during the back-to-school shopping season, it’s predicted that 2023 will experience another subdued peak season.”

“Smaller trucking fleets are facing financial pressures due to declining spot rates, high interest rates, and a 20% increase in diesel prices since July.”

Let me summarize: despite all the recent fall in demand and the resulting decline in prosperity, the price of diesel just keeps rising. Keep this in mind. Then have a look at this one:

OPEC Cuts Reignite Inflation Worries As Energy Prices Rise

“The International Energy Agency warns of a deepening oil market deficit in the fourth quarter due to extended Saudi and Russian production cuts.”

“Diesel shortages are affecting sectors such as construction, transport, and farming, with global inventories significantly below the usual levels for the year.”

“Despite President Biden’s promises to reduce gas prices, options like the strategic petroleum reserve are dwindling, and increasing production is not an immediate solution.”

Perplexing? Hardly. No cheap and abundant energy — no economy. On the face of it all this could be explained by OPEC production curbs and the resulting fall in diesel inventories. However, if you look at the long term trends of stagnating / falling prosperity per capita, while fuel prices keep rising and rising, it’s not hard to see that the world is grappling with a structural middle distillate shortage... For more than a decade now. Not because of a pandemic, a war or economic hardships. The reason is an inadequate production of conventional, cheap to extract, medium heavy sour crude oil — the most ideal feedstock for making diesel fuel from. Ever since 2005 the production of this valuable substance has been flatlining. On top of that, the 2020 crisis saw many old (conventional) wells closing permanently, only to be replaced by fracked tight oil, yielding much less diesel per barrel than medium heavy oils coming from old extraction sites.

Saudi Arabia, home to the world’s largest oil fields producing just this type of oil, is another case in point. As their old, close to surface, cheap to produce giant fields keep declining, Saudi Aramco too is forced to replace production with more energy intensive to drill and maintain smaller / deeper fields. Is it any wonder then that their breakeven oil price rose to $95 a barrel, as per an estimate from Bloomberg Economics?

It takes energy to get energy. Since the oil industry is now hopelessly dependent on other sources of energy to prop up “production”, higher overall energy prices push oil extraction costs even higher. Unconventional sources, replacing old wells on the other hand, require a thousand truckloads of sand, water and drilling equipment to be brought on site — via diesel… What else? This is not to mention all the extra coal burned in smelters and steelworks making all the pipes, or the natural gas converted to electricity to run the equipment — and the list goes on. The proposed replacement for waning medium heavy oil production (ultra heavy oil either from Canada or Venezuela) takes even more energy to extract and refine, requiring a permanently high oil price to be viable. Bio-fuels are also not an option, as crude would have to hit ~$500/barrel for the much touted algae biofuels to compete successfully, while soy based agricultural fuels are taking away farmland from food, beside requiring a ton of diesel to cultivate, water, harvest and deliver to a processing plant (thus adding little to none to overall diesel fuel availability).

Higher oil prices also tend to push inflation even higher, prompting interest rate hikes and lower consumption, effectively curbing production growth and further aggravating the woes of the transport industry. Again, we are in a situation where oil prices are still not high enough for producers, while consumers simply cannot afford to pay more. Rising oil prices above a certain level start to act like a brake on the entire industrial world, though, not an incentive to drill more. Is it any wonder that the Saudies do not see a supply deficit and keep to their production cuts?

Big oil will blames all this on bad policies and the lack of investment, supposedly taken up by ‘green’ technologies, but this is just playing the blame game. If this were true, big petro-states, who could not care less about climate change, were investing heavily and outproduce everyone to meet demand. As we have seen, though, this is far from being the case. In reality a growth in oil production has got too energy intensive to maintain — and thus a decline is inevitable. Notwithstanding all those proven reserves and high resources (theoretically lasting for decades more), oil production will start to dwindle due to its failing energy economics.

What this will mean in practice, is that less well-to-do customers will be simply priced out of the market, through their inability to afford previous consumption levels. As a response producers will keep reducing production in anticipation of lower demand, and in order not to allow prices to fall below breakeven levels. As cheap to produce fields keep declining though, and as these have to be replaced with ever costlier to extract ones, so will the breakeven price rise ever higher. The circle of potential customers will thus keep shrinking even further, prompting a further cut, which in turn raises prices even higher leading to even lower consumption and to another round of production cut. Rinse and repeat. This is how endless expansion turns into an ever faster downhill ride; seeing the idea of ‘endless progress’ and ‘infinite growth on a finite planet’ flying out the window in slow motion — towards the compost heap of history.

Until next time,

B

Thank you for reading this post. If you would like to see more in depth analysis of our predicament, please subscribe for free — and if you can afford it, consider supporting my work by opting for a paid subscription or taking a snapshot of this QR-code (or by clicking the link below). Thank you!

Notes:

In the US only 4% of households use heating oil still — taking up only 9% of total distillate fuel oil use. Although their numbers are falling year after year, they do so with a small percentage only: making this change insignificant compared to fluctuations in diesel (road transport) use. For avid data miners here is another great data source — have fun!

Thanks for all your writing efforts, appreciated, and glad to read you quoting from Dr Tim - his SEEDS model is invaluable. There is a cadre of like minded de-growth writers I hope this growing collective voice is heard more widely.

Thank you B🙏