Infinite Growth Delusions Continue - For Now

When conflict of interests meets reality

According to the data published in the latest release of the Statistical Review of World Energy, infinite growth continued unabated in 2025—this time with “renewables” at the helm. But what is underpinning this unabated growth in energy consumption? Do we have the resources needed to continue with this trend? According to the report—or at least to the message it tries to convey—the answer is a resounding ‘Yes, without a doubt.’ In fact, and as you will see from the data presented below, the opposite is true: the world economy is facing a complex predicament, which will force it to contract—regardless how we wish “renewables” and batteries could save the day, and no matter how this paper is unwilling to concede to the simple arithmetic behind. A fact based critique is in due order.

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

Stories we tell ourselves

According to the newly released report, total energy supply in 2025 increased by 1.7% over the previous year, with solar power accounting for the vast majority of this growth. Despite solar’s rapidly increasing share of world energy—now at 8.7%—all other forms of energy use continued to expand in absolute terms, including fossil fuels. Coal, oil and gas use have all increased throughout 2025, and still accounted for 86% of all energy supplied to the economy. Contrary to the stories we tell ourselves the energy transition still hasn’t started yet: wind and solar are still mere additions to an ever growing pile of carbon based fuels.

Beside providing the raw data (in a downloadable format) the report also imparts “insights” into the world of energy; short narratives intended to plant stories in the heads of executives, government officials and consultants on where the world is headed and what to expect in the future. No wonder: the report was written and backed by some of the biggest names in business consultancy—a clear conflict of interest. And while the data with its narrow interpretation is spot on—as always—the general audience is still left missing the big picture. These stories—deliberately or not—often omit and overlook very important aspects of energy use and supply, even though its right there in the data—if you know where to look, that is. Instead of providing the reader with an honest assessment on the state of the world economy and its future prospects, authors of the Statistical Review are building a bridge to nowhere, based on a blind faith in infinite growth on a finite planet.

Perhaps the best example of this is Insight 2: Energy security in a changing world — How the 1970s oil shocks shifted energy patterns (page 8-9). After misidentifying the problem as an issue rooted solely in politics and war, while forgetting to mention that the then largest producer and consumer of oil in the world by far (the US) has passed it’s own domestic peak in conventional oil production in 1970, then suffered a 15% drop in output making its economy extremely vulnerable to external shocks, the report suggests that the crisis was eventually solved by other sources of energy (coal, gas, nuclear) taking up the slack. While the reference to the present crisis around Hormuz is not explicitly there, it is very hard to miss: ‘Don’t worry so much about oil, solar is here to save us!’

See, had the United States been able to continue growing its oil supply in the same manner it did before 1970 (that is at a 7% year-over-year growth rate), it could have easily kept itself and its allies well supplied—OPEC embargo and the Iranian revolution notwithstanding. Since it couldn’t, though, no matter how hard their oil companies tried, the US increasingly became import dependent—making its economy extremely vulnerable to interruptions in supply. Hence the unprecedented price hikes with long lines at the pump, prompting car manufacturers to invest in fuel efficiency measures, and urging power plants to ditch oil as a fuel source. In summary: the oil intensity of the economy and the rate of oil extraction growth fell not because we no longer needed oil, but because we could no longer increase its rate of extraction.

This limitation in oil supply—partly imposed by geology and partly by the economics of oil extraction itself—significantly reduced economic growth and led to a severe double-dip recession in the early 80’s, followed by stagflation and the secular stagnation of the 1990’s. It wasn’t until the neoliberal policies of Reagan and Thatcher, with their rampant financialization, privatization, outsourcing and an explosion in debt (both private and government), till GDP growth finally returned. The loss of cheap energy, however, has also meant the loss of heavy industries and car manufacturing. But as long as cheap imports kept flowing into the West from the far East, the simulacrum of growth in the West could continue—for a while.

What the data tells

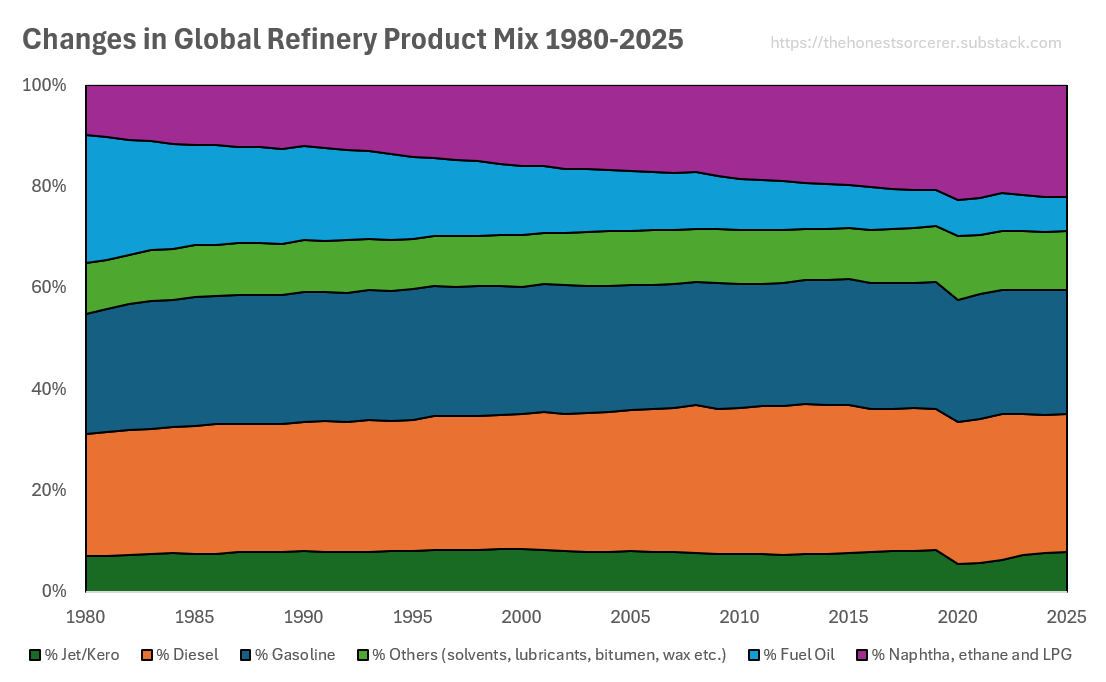

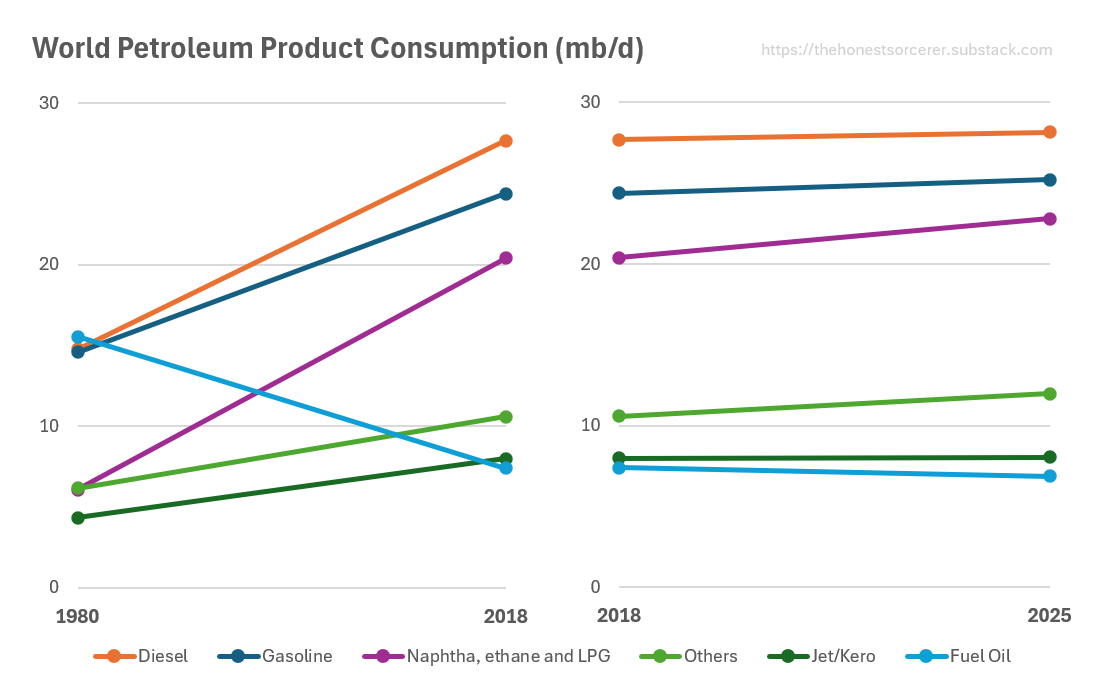

So, what does the data, provided in the Statistical Review tell us about this story? Can we pull off the same trick of the 1980’s again? Looking at Oil Regional consumption by product group a number of slow changes in oil use over the decades becomes visible. After the dual shock of the 70’s refineries increasingly focused on making more diesel and gasoline from the same barrel at the cost of “sacrificing” fuel oil. In 1980 roughly a quarter of a barrel was refined into gasoline globally, another quarter found its way into diesel fuel, while slightly more than a quarter was burned as fuel oil (marine fuels and crude oil directly used in power plants). The remaining part was turned into jet fuel, naphtha, solvents, lubricants, bitumen, wax etc.—essential inputs needed by the wider economy. Over the 1980 to 2018 period, however, oil’s use as a fuel has shrunk to a mere 7%, while refineries were still turning half of each barrel into road fuels and a steady 7-8% into jet fuel.

What made the situation particularly challenging was the relentless rise in the share of Natural Gas Liquids (NGLs) in what statisticians call oil. You see, not everything is oil, what is marketed as such in the Statistical Review: a growing portion of the barrels consumed around the world is increasingly coming in the form of ethane, naphtha, propane and butane. These substances are produced mostly as a by-product of processing natural gas (hence their name) but have very little to do with the real thing: a thick brownish-black liquid called crude oil. And while NGLs can still be used as precursors (raw materials) in manufacturing plastics and for filling cooking gas cylinders—they have little to no use in making more road and aviation fuels.

In the end this refinery optimization process, combined with a growing share of NGLs in the mix, has led to an almost complete cannibalization of the ‘fuel oil’ category (light blue on the chart), prompting power plants to essentially stop burning oil and thus leaving very little room for future adjustments. As you can see, this is a one-way street: once all crude is refined to gasoline, diesel, jet and bunker (shipping) fuel, plus a range of other essential products, there is no oil left to be substituted with other energy resources. Especially not in a world where most of the additions to global ‘oil supply’ comes in the form of volatile super light matter condensed from natural gas.

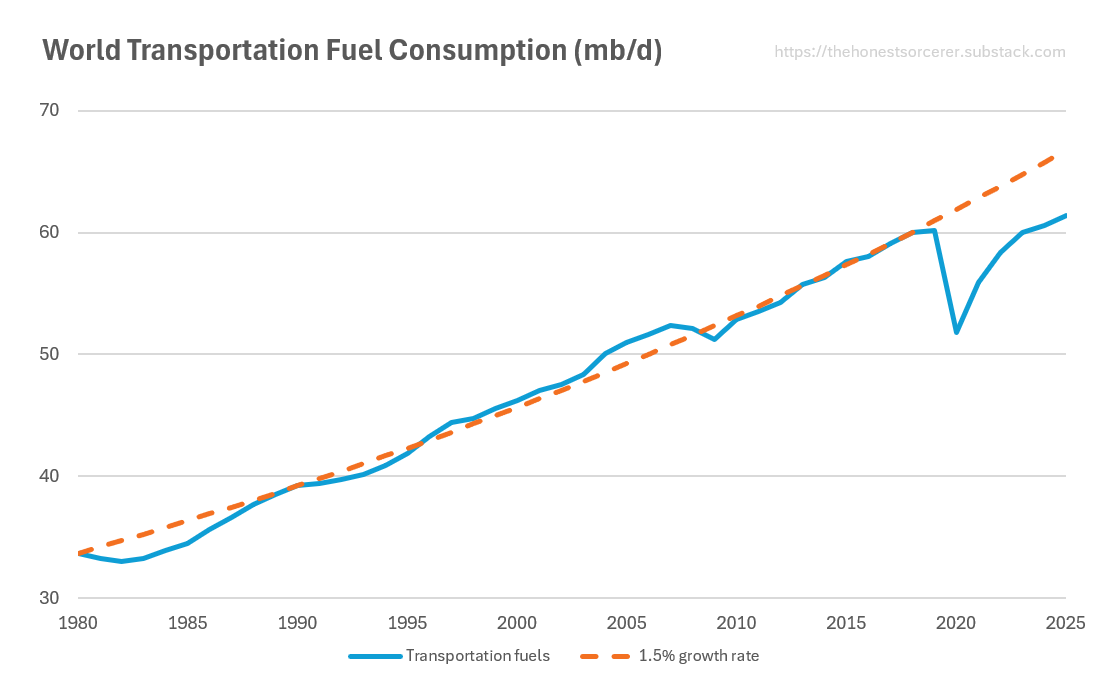

As result increases in the global consumption of transportation fuels (gasoline, diesel and jet fuel) have become strictly limited by the amount of “real” crude oil we could add into the mix. Consequently growth in fuel supply was capped at an average rate of 1.5% per annum from 1980 up until 2018, closely following increases in world crude oil supply. Then something broke—a full 2 years ahead of the pandemic. Make no mistake, I do not mind at all if we drive and pollute less—in fact doing away with burning so much fuel would be much better for the living world and the planet as a whole. That trend breaking, however, is totally incompatible with the expectation of infinite material economic growth. See, a physically growing world economy requires more mining, more agriculture, more construction, more goods delivered etc. by definition. In other words: higher oil and especially higher diesel fuel consumption. That kind of growth, however, is nowhere to be seen since 2018: based on the amount of fuel burned, the world economy has barely managed to climb back to where it was eight years ago.

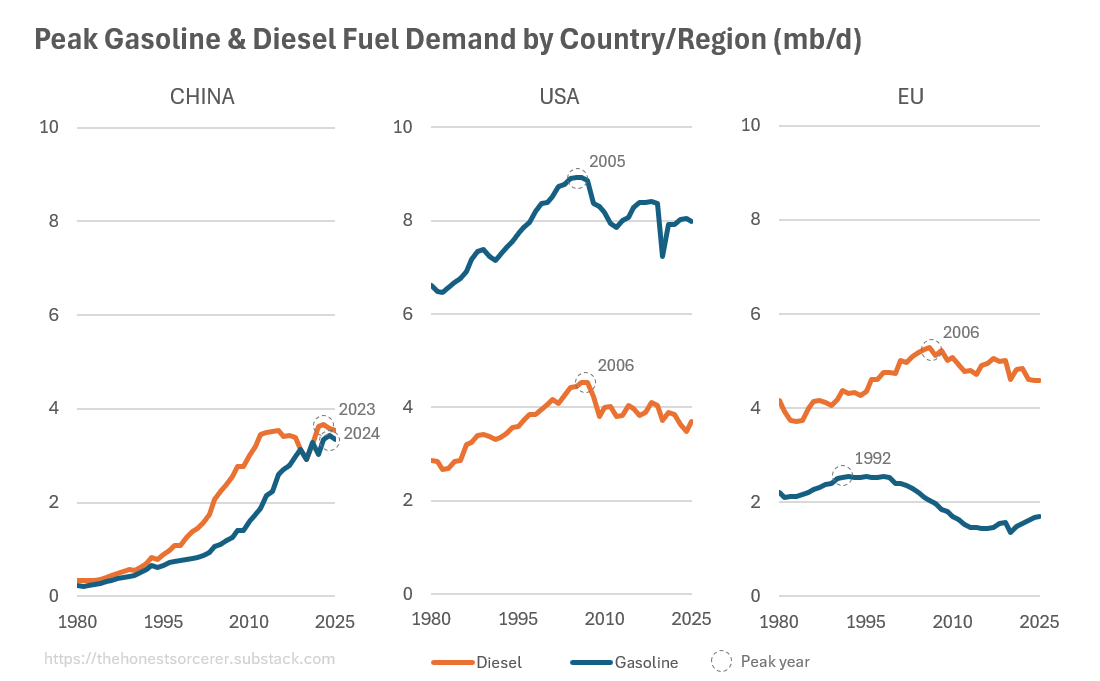

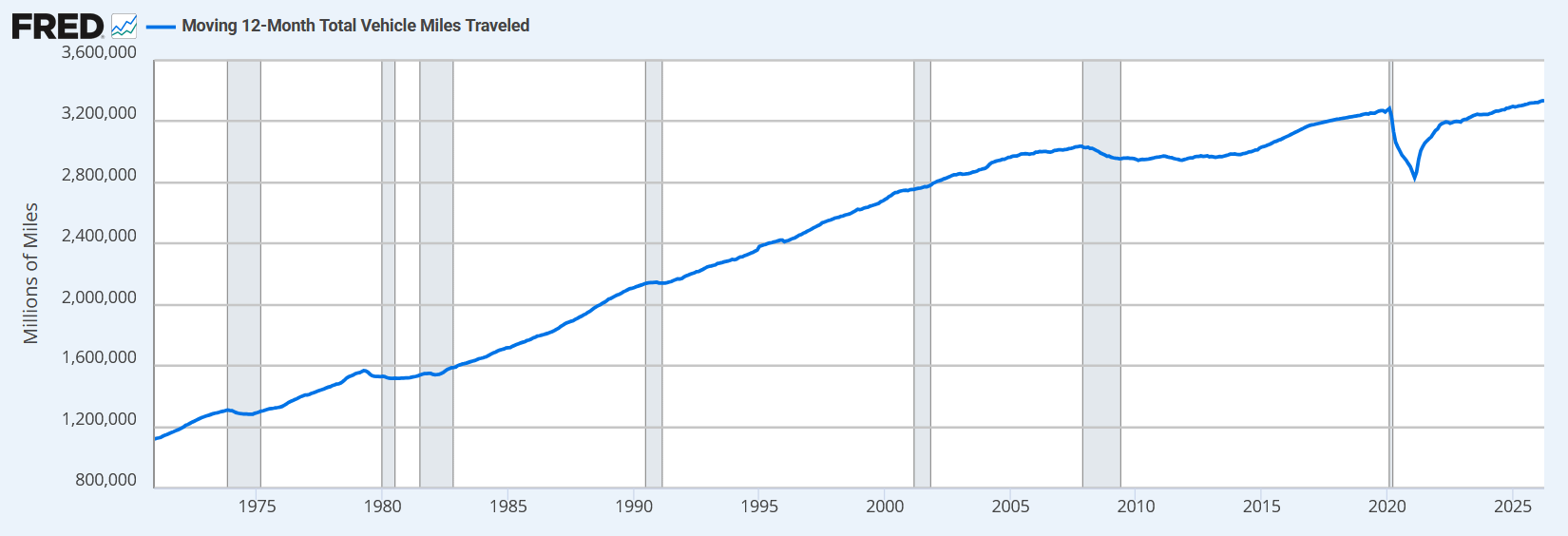

Despite Chinese efforts in weaning themselves off of diesel trucks (by increasingly switching to LNG and battery electric medium and heavy duty vehicles), diesel consumption is still one of the best global indicators of real economic activity. Just take a look at the consumption habits of the three biggest economic blocs of the world—responsible for 48% of world GDP in aggregate—and see how their fuel consumption fared in the past 45 years. Notice, how all of these three centers of economic growth have all peaked in road fuel use well before electric vehicles became a thing. Observe the massive drop in fuel consumption in the West right after their peak in 2005/2006, and while at it don’t forget to take a look at how the Chinese growth miracle has ended abruptly in 2012. Again, how many electric vehicles were on the roads back then?

Sure, increases in fuel efficiency did play a role, you could say, but then take a look at the millions of miles driven in any 12-month period and the picture becomes clearer. The economic crisis which followed the 2008/9 financial crisis, the persistently high fuel prices, job losses and a general fall in consumer sentiment made sure that neither diesel, nor gasoline demand could return to their previous levels, let alone to a steady growth trajectory seen before 2006.

Simply put: the great financial crisis—itself triggered by a worldwide peak in conventional (onshore, close to surface and shallow water) crude oil extraction in 2004/2005, and the subsequent rally in oil prices—broke the back of western economies. Even as aggregate world crude oil production haven’t peaked yet, just the most valuable part of it, it was enough to put a definitive end to decades of industrial output growth in the West. No amount of shale oil, tar sands or natural gas liquids managed to change that picture, as these unconventional sources of ‘liquids’ came at a much higher cost of extraction and were much less useful to the economy. At the same time the frantic drilling and fracking of ever faster depleting wells began to cannibalize diesel fuel and electricity flows, eating away these valuable energy sources from the rest of the productive economy. So while in 1980 every barrel of oil equivalent (boe) energy invested into drilling resulted in 30 new barrels recovered on a global average, this number is well below 10 by now, meaning that more and more energy needs to be reinvested into getting energy, leaving an ever smaller surplus for the rest of the economy.

And if that weren’t enough—or rather: as a result—global car sales also peaked in 2017, just like demand for trucks, which has fallen 20% since then. Global steel production, requiring massive amounts of iron ore, coal and finished products to be delivered on trucks, ships and trains, has also peaked five years ago, in 2021 already. No wonder that there is little demand growth for fuel, as life itself became more and more unaffordable to many—a trend reinforced by the pandemic and the many subsequent wars fought over domination and ultimately over resources. So no, the drop in fuel demand you saw above was not a result of electrification1, but a consequence of long term trends finally bearing fruit. No (real) economic growth, no new fuel demand either—no wonder Chinese and Asian oil imports fell so much lately.2

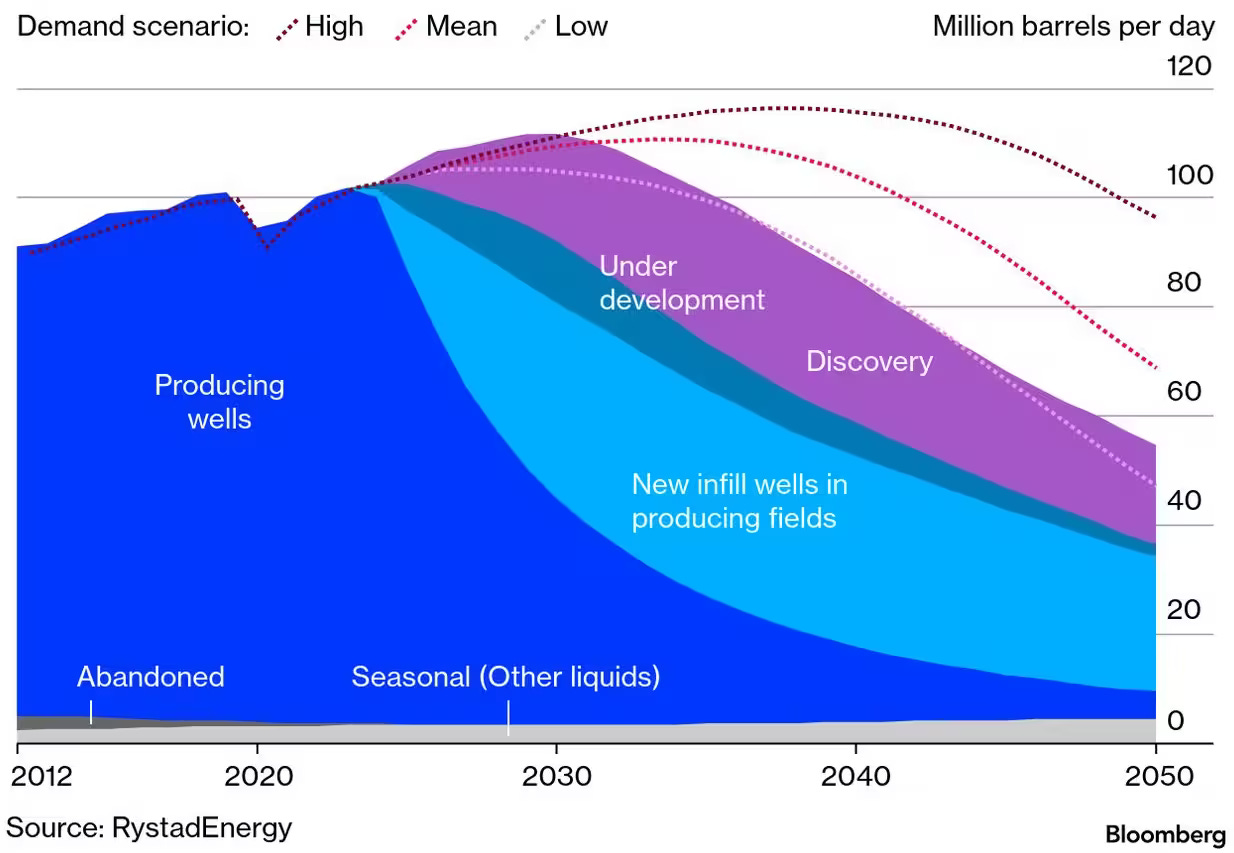

Meanwhile these trends haven’t stopped global peak oil supply on its tracks, only made that steady drop in oil output less painful when it arrives. If not, high prices will make sure we all drive—and more importantly—consume much less as the decades march on. If Rystad’s estimates are correct, about a half as much oil will be available than today by 2050… Food for thought. So why is this alarming trend not discussed in the Statistical Review? Why have they removed the state of proven oil reserves from their report? Because, perhaps, these reserves stopped growing and had to be revised downward? Well, according to Rystad Energy this is precisely the case—too bad they, too, have removed this information from their website later (here is an archived version):

“Global recoverable oil resources, including estimates for undiscovered fields, stabilized at approximately 1.5 trillion barrels. The most significant revision over the last 10 years has been in yet-to-find resources, where our projection has been reduced by 456 billion barrels. This is due to a steep decline in frontier exploration, unsuccessful shale developments outside the Americas and a doubling in offshore costs over the past five years. Rystad Energy expects reserve replacements from new conventional oil projects to be less than 30% of production over the next five years, while exploration would replace only about 10%.”

Another study from the IEA, published last year, found that as oil fields mature (read: deplete) production decline accelerates. At first just by a little, which can be easily offset by enhanced oil recovery techniques, then ever faster and faster… Till the increased energy and material investment needed to keep the juices flowing no longer worth it, and extraction stops. Bad news is that, in 2024, around 80% of global oil production and 90% of natural gas production came from fields that had passed their peak in production (including unconventional wells). But, of course, we don’t talk about these things, as they are bad for business… We are consultants after all, and the belief in infinite growth must be upheld at all cost—no matter how unfounded it is.

Conclusion

Needless to say, this does not bode well in our present situation, with traffic through the Strait of Hormuz still well below the historical average; endangering diesel supply around the world and threatening with a major economic downturn. See, there is not much wiggle room left in the oil industry: apart from a few lucky regions oil production has already peaked in many places around the world, and we are not far off from an absolute peak in global crude supply either. Fuel switching—as vaguely suggested by the Insight story I discussed above—will not work this time either, as large cargo ships and bulk carriers badly need the remaining portion of fuel oil. There is nothing left to be sacrificed: if oil production falls—either due to wars, or due to a global peak in production whenever it comes—the economy falls with it.

Diesel fuel, the most valuable portion of the barrel cannot be substituted with electricity at scale either, as agriculture, mining and long distance trucking (not to mention construction) are still completely dependent on this fuel. And without these activities, there is no copper, zinc, nickel, silicon—or anything needed to make “renewables” plus the gazillion electric devices, batteries, transformers, high voltage lines etc. needed to build a ‘smart’ grid to accommodate them. Average citizens buying electric vehicles will not and cannot change that picture—only worsen it by hasting mineral depletion. (In fairness the same goes to driving gas guzzlers.) See, contrary to the impression conveyed by the authors of this report various energy sources are neither fungible beyond a certain limited degree, nor infinite: as each depend on mining non-renewable resources to depletion.3

So, despite the fact that oil production and consumption have climbed to new record highs in 2025 (surpassing the previous record set in 2018)4 one cannot ignore the dark clouds gathering on the horizon. Even if traffic eventually normalizes through Hormuz, and Latin America, Libya and some other nations keep pumping more oil than they ever did, the rising energy cost of drilling and delivering more oil, together with natural decline throughout the rest of the world will eventually tip global crude oil (and then natural gas) output into a long enduring decline. Not just the conventional part (as it happened in 2004) and not just in one country (the US in 1970)5—but on a global scale. I wonder whether that will be the year, when this series of the most widely respected publication in the field of energy economics, the Statistical Review of World Energy, finally comes to an end.

Until next time,

B

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

Even in China, the poster child of electrification, EV sales fell by 9% and overall car sales declined by a sizable 22.3%—indicating that the true cause behind a fall in gasoline sales is an economic slump, not a booming EV market… And the same goes to Chinese truck sales, just sayin.

In 2025 India imported 86% of its oil consumption while China and Europe imported 73% and 75% respectively. Chinese oil imports increased by 3.4% to 13.9 mb/d in 2025 and crude oil stock levels reached an estimated 1.4bn barrels by the end of last year.

Fun fact: if you scroll down to the bottom of the Statistical Review report, you find the R/P (reserve to production) ratios of various metals needed for the transition. Of particular interest are cobalt (42 years of present day production left in reserves), copper (43 years), nickel (39), and finally zinc (19!). Note also, that none of these reserves could be recovered at the present rate of production: as mineral resources deplete and one mine closes after the other, production peaks then begins to decline. I wonder when these metrics will (too) be removed from the report…

Crude plus condensate extraction (oil in the traditional sense of the world) has hit a daily average of 85.76 million barrels a day in 2025, surpassing the previous record set in 2018 at 83.6 mb/d. At the same time total liquid fuel and petroleum product consumption has surpassed 106 million barrels a day, thanks to a record high natural gas liquids production and all those biofuels, coal-to-liquids, “refinery gains” and the rest of the gunk finding its way into the statistics.

Despite a recent rise in oil output in America, “U.S. oil production will peak at 14 million barrels per day in 2027 and maintain that level through the end of the decade, before rapidly declining”—according to the U.S. Energy Information Administration as reported by Reuters.

Sad isn’t it, that after all this time, since the 70s, we’re still in denial. Wait till we get to anger, which is what comes next. People today might be angry at one side or another politically, but wait til they discover there’s no way out of our predicament no matter which side you’re on.

I agree with your analysis. Initially, renewables offered a concrete path toward sustainability, but they have devolved into just another narrative—a comforting myth designed to make the status quo more acceptable as we decline.