Europe's Downward Spiral Accelerates

Europe is in trouble. After struggling with high energy prices and stagnating then falling demand for three years in a row, companies have run out of leeway. Now, we are witnessing the effects of a chronic under-consumption crisis and a loss of competitiveness on a historic scale. This is not your run-of-the-mill economic downturn from which there is a quick rebound. In fact, the basket case of Europe has provided us with a preview what the relentless rise of the energy cost of energy means for the economy, and ultimately for industrial civilization as a whole. Rest of the world: take notice.

Thank you for reading The Honest Sorcerer, and special thanks to those who already support my work: without you this site could not exist. If you are new here and would like to see more in depth analysis of our predicament, please subscribe for free, or perhaps consider a paid subscription. You can also support my work by virtually inviting me for a coffee, or sharing this article with a friend. Thank you in advance!

Deeply indebted, cash stricken and burdened with overcapacity European companies have no other choice left than to start dismissing their workforce. German companies in the Fortune 500 Europe have announced over 60000 layoffs this year alone. The auto industry is especially hard hit: as discretionary spending falls throughout the continent, and as Chinese competitors increase their market share worldwide, demand for European made cars plummeted over the past years. This is not the end of the story, however. A recent bout of energy inflation (especially in wholesale electricity prices) signals that the crisis is far from being over.

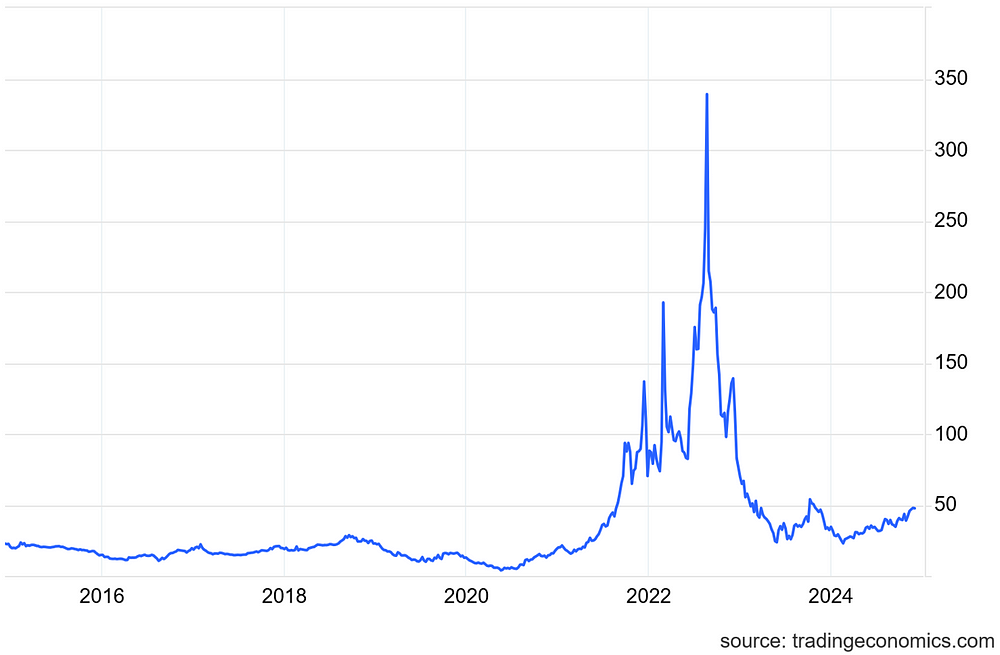

What started as a “failure” to meet the energy demands of a post-COVID rebound, has now turned into a full blown energy crisis unwilling to recede. As lockdowns eased and economic activity returned in 2021, demand for natural gas has increased substantially worldwide. Many oil and gas wells — shut-in during 2020 — on the other hand, could not return to full production and as a result a natural gas price rally began; half a year earlier than the fighting in Ukraine escalated into an all out war.

Fighting alone had little effect on the price of natural gas in Europe, though. Various sanctions, lawsuits, asset confiscations and seizures, abrupt withdrawal of permits, “mysterious” pipeline explosions and denial of payments from the European side, on the other hand, had a significant role to play in the rally depicted on the chart above. Just for context: before the war Germany used to import 50% of its coal, 55% of its natural gas, and 31% of its crude oil from Russia, representing 33% of Germany’s total energy consumption — all of which falls under some sort of sanctions today. Now, with the exclusion of Gazprombank, the bank handling most of the international transactions for Gazprom (the largest gas producing company in Russia) from the SWIFT inter-bank messaging system, and Ukraine unwilling to renew transit permits through its territories, the cheapest form of natural gas supplies to Europe will likely dwindle to a mere trickle. That will leave Europe with expensive LNG from Qatar and the US, as well as some pipeline gas from Norway and through Turkiye, which is Russian gas in a roundabout, third-party way. As always: higher complexity comes at a higher price — a direct consequence of the EU’s economic war on its largest energy supplier.

Will this lead to a repeat of the 2022 price rally then? Hardly. As one can see from the extent of layoffs cited above, Europe is deindustrializing fast. Half of the continent’s steel, glass and aluminum capacity, together with fertilizer and chemical plants have already left in the first wave (in late 2022 and early 2023). Now, it’s time for the automotive and machine manufacturing sector to go, together with the “renewables” and battery businesses. Well, energy is (still) the economy, it seems. As industrial demand recedes, however, so does consumer demand. With mass layoffs, and in response to a huge drop in the purchasing power of their money, people started to buy less and less products made with expensive energy, and turned down the heating in their homes even further. (Read Tim Watkins’ excellent account here on the monetary consequences of this crisis of under-consumption.)

Despite the disappearance of cheap gas from the market we will neither see another price rally, nor run out of gas by the end of winter. It will not be a smooth ride though. Were it not for “renewable” energy, we would “only” see a slow dying of the natural gas intensive part of the economy — which is still a big deal on its own. With the predictable unpredictability of wind and solar, however, and with a massive reliance on natural gas fired power plants to balance electricity demand, Europe has just saw the fastest drop in natural gas storage in years. Yes, the weather was cold in the past couple of weeks, but it wasn’t nearly as cold as it could get in the dead of winter. Wind on the other hand stopped blowing, which not only resulted in lower electricity generation from wind turbines, but also in thicker clouds and more persistent fog… Leading to a much diminished solar power generation. Welcome to the good old Dunkelflaute (or the dark doldrums) so common this time of year, and by the way sometimes throughout the entire winter... Who could have thought that “renewables” produce much less electricity during wintertime…? Or that pushing more and more households and businesses into using electricity for heating (via heat pumps) could backfire in such a situation?

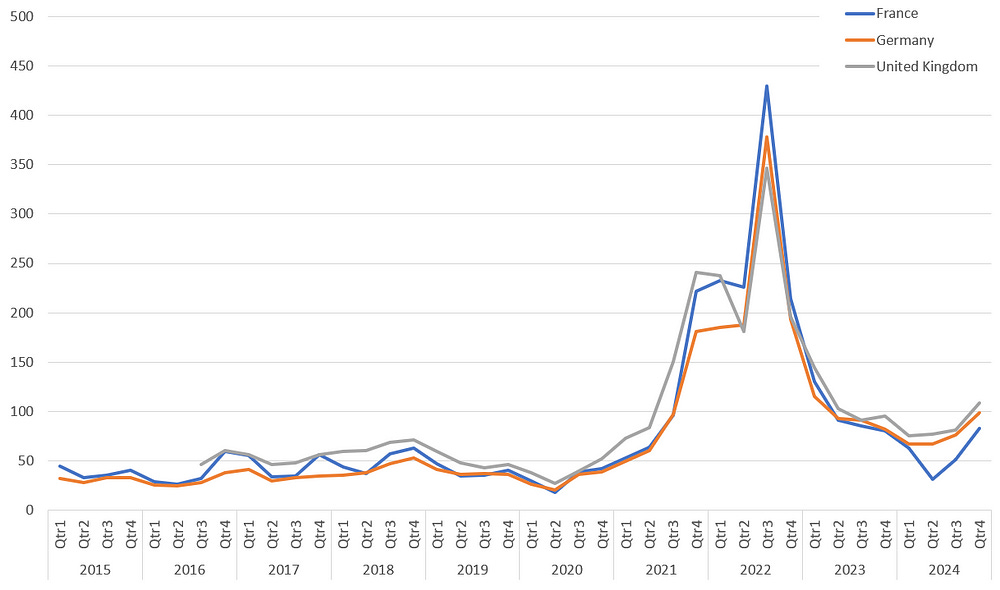

The lack of cheap pipeline gas in combination with an ever increasing share of “renewables” has led to a sharp rise in electricity prices all across Europe. How this will affect the electrified part of the economy is anyone’s guess at this point, but the fundamentals do not look good, at all. Europe lacks an adequate domestic supply of hydrocarbons, even as its economy remains heavily reliant on natural gas and diesel oil. One third of the EU’s energy still comes from abroad, making it the most energy dependent region of the world — irrespective of sources. Now, that an extended drought has lead to a diminished hydroelectric power generation in the Mediterranean and Scandinavia, the return of low electricity prices seem highly unlikely.

Oddly enough the situation would not improve even if the wind begin to blow again. While Europe has still grossly inadequate “renewable” energy capacity to replace coal and gas (especially during dark winter days), it has more than enough to cause widespread disruptions to the grid once the sun begins to shine or when wind speeds pick up again. Whenever a large solar farm returns production it sends a shock wave through the grid, damaging sensitive equipment nearby. Similarly, when a cloud suddenly blocks the Sun a micro-blackout could occur (lasting a few milliseconds) till back up capacity comes online. These fluctuations in the supply of electricity has forced many companies with sensitive manufacturing equipment to install surge protectors and uninterruptible power supply units costing tens or hundreds of thousands of Euros (depending on size) or outright buying a natural gas powered generation unit to produce their own stable electricity supply. Needless to say, these actions made them less cost competitive than other manufacturers enjoying a stable grid, and forced them to push their increased costs onto their customers.

There are more hidden costs when it comes wind and solar though. Since these sources do not produce when power is needed, overproduction forces the grid operators to curtail these power plants. Due to the high upfront investment needed to build “renewables” though, a compensation scheme was devised costing UK consumers, for example, £1.3 billion this year alone. Addressing the curtailment problem, contrariwise, would require a costly grid expansion, estimated at £40 billion — annually. “Renewables” thus not only cost a ton of money (as well as energy and resources) to build, and cause headaches to owners of sensitive electric equipment, but require active compensation should the sun shine too much or the wind blew too long. Meanwhile if it’s dark and windless outside costly LNG must be burned to compensate for the loss of power, causing a spike in electricity prices. Again, this is nothing new: the physical characteristics of these devices were known for more than a century now, and the economic consequences (laid out above) were also clearly demonstrated more than a decade ago (Hirth, 2013).

Despite all these facts, the policy of weaning Europe off of (Russian) fossil fuels was pursued with religious fervor. In order to compensate businesses somewhat for the predicted rise in energy costs, and in hopes that these “problems” wont last, a system of subsidies were implemented. Contributing to companies’ and households’ soaring energy bills for such a prolonged time, though, could not be sustained without going into debt. Now the chickens come home to roost. First the German, then the French government (two of the biggest economies in the EU) collapsed over debates on soaring debt levels and deficit spending. Again, no (cheap) energy, no economy. No economy, no consumption, no tax revenues. Irrespective of who is called the next chancellor or prime minister, he or she will have to deal with a massive debt crisis, and in case of France, an even bigger one than that of Greece’s in 2009. In the meantime, and just for the record, the IMF has just named Russia the 4th largest economy of the world, surpassing Japan and Germany; after the World Bank classified it as a high income country. Despite all protestations, sanctions actually helped Russia rein in its worst oligarchs and encouraged investments to replace lost imports. Contrary to what Europe’s ruling elite had in mind, their policy has lead to a huge economic boom in Russia, driven by internal consumption and powered by an abundant supply of fossil fuels. (This is not to say that Russia’s resources will last forever, but certainly much longer than that of the West’s.)

The question — no one dares to ask — poses itself: With a rapidly deindustrializing economy, combined with a similarly steep fall in consumer spending and structurally high energy prices, how on Earth should Europe pay back its debts and return to prosperity…? The question, of course, is only rhetorical. Europe has entered a death spiral, and its very hard to see how (or rather if) it can escape its fate. The continent’s predicament span much further than its shorelines, though. As the energy cost of energy (1) keeps increasing worldwide (not just in Europe), even currently prosperous regions will stop growing and face a long decline in living standards. Modernity was based on a finite amount of easy to access fossil fuels and mineral wealth, something, which not only causes climate change but is running out rapidly as we speak. Is it any wonder that we see a mad scramble for remaining resources?

In light of the above it’s even harder to understand how European elites could be so irresponsible. Instead of revising their energy / foreign policy, they have doubled down on “renewables” even as they severed all vital links to their primary source of cheap fossil fuels. Contrary to its vital economic interests, Europe has tied its import dependent economy to a fast sinking “rules based world order”, together with LNG supplies from the U.S. with diminishing reserves and a soon to be peaking production. Instead of doing everything to prevent a war with their biggest neighbor, and to find a cooperative coping mechanism to deal with the coming long decline in world energy production, the EU and NATO remained hell bent on expansion and sabotaged every deal along the way — together with the many opportunities for peace. Even as the war is being lost as we speak, there are still no talks about building a lasting peace taking both side’s security considerations into account. Instead, we hear more ‘peace through strength’, ‘deterrence’ and sending European troops into Ukraine to freeze the conflict… Only to prepare the country for a renewed offensive few years later. Just like many times before in the old continent’s battered history confrontation was chosen over cooperation, ultimately leaving Europe in ruins and in a deep economic turmoil. Only this time, in the absence of a cheap and abundant new energy source, the downturn could all too easily become permanent.

Until next time,

B

The Honest Sorcerer is a reader-supported publication. Please consider a subscription or perhaps buying a virtual coffee… Thanks in advance!

Notes:

(1) The energy demand of extracting oil increases with every year and easy-to-access wells will increasingly be replaced with costly, hard to reach, deeper than ever ones further and further away from civilization. Thus the time will eventually come when boring the next hole will simply not worth it: oil will become too cheap for companies to extract, while at the same time too expensive for consumers to continue using. Eventually, economies not so rich in easy to extract oil will find themselves in a severe competitive disadvantage and begin to contract unstoppably, reducing demand and prices alike. This would, of course, lead to further curtailments in production, leading to further consumption cuts (elsewhere). Rinse and repeat, and viola’ a permanent decline to the world economy presents itself. Mind you, this has nothing to do with politics or money: the decline of cheap fossil fuels was baked into Earth’s geology millions of years ago. The only choice we have is how we adapt to this reality, not how we turn it around.

I usually follow your posts with interest, but once you talk about 'Europe' as though it is one country and one economy, then you've lost me. Europe is 27 countries in the European Union. Is that what you mean?

Or do you mean the 44 countries in Europe, including the ones that are not members of the EU?

Or do you mean the 20 countries using the Euro as their currency?

Do you include Britain, that is in Europe but not in the EU? And what about Ireland, close to Britain but in the EU, except for the northern part which is half in, half out of the EU and politically part of Britain?

And then there are northern and southern European economies, some Mediterranean ones with lots of sunshine that are producing lots of solar power, and some northern ones that are producing lots of wind energy, and of course electrified France with 70% nuclear and 15% hydro, that sells excess energy to Germany, Britain and Spain, so is barely affected by fossil gas prices.

If you want to give opinions about the dire state of Europe, I think you need to be MUCH more precise and accurate about where exactly, and why, for your very general opinion-from-a-distance to carry any weight.

We're witnessing the death throes of capitalism. Hang on because it's going to get worse😞