Peak Steel

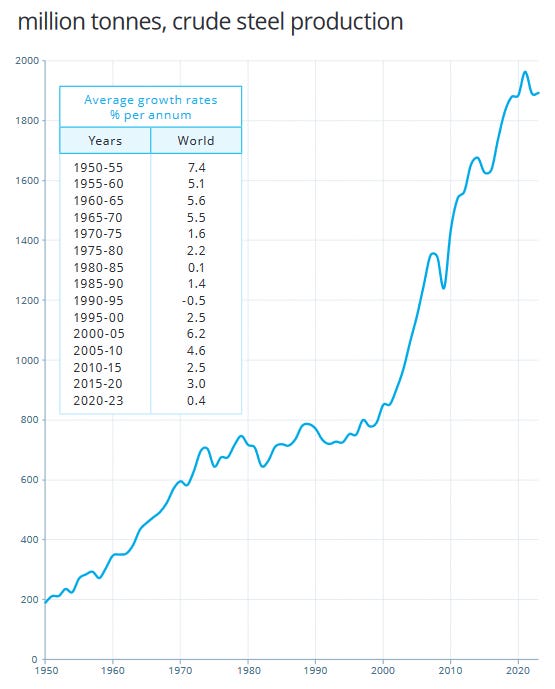

Global steel production has peaked in 2021 and it's stagnating ever since. Is this just another minor hiccup or an ominous sign of a much bigger crisis in the making?

There is a saying, attributed to Stalin, that “quantity has a quality of its own”. And if there is an area of life where this is most certainly true it is steel production. This metal is literally everywhere: from cars to kitchen utensils, from computer housing to hard disks, or from bridges and pipelines to tanks and warships. It’s perhaps no exaggeration to say that without steel there would be no such thing as modernity. There is a problem however: global steel production has stopped growing in 2021. Now it’s back to 2020 levels, producing the longest period of zero growth since the early 90’s (the fall of the Soviet Union). Are we seeing a return to the great stagnation of the 1975–1995 interval, when crude steel output barely grew for decades, or is this just one of those hiccups in global production growth? I suggest we are seeing another side effect of plateauing oil production, but let’s not get ahead ourselves just yet.

Thank you for reading The Honest Sorcerer, and special thanks to those who already support my work: without you this site could not exist. If you are new here and would like to see more in depth analysis of our predicament, please subscribe for free, or perhaps consider a paid subscription. You can also support my work by virtually inviting me for a coffee, or sharing this article with a friend. Thank you in advance!

First let’s start by understanding the role steel plays in our modern lives and how this material is made. Just to illustrate the humongous amount of steel produced worldwide (around 1890 million tons annually) imagine 27,000 Nimitz-class aircraft carriers rolling off a production line every single year. That is 3 vessels every hour, 24/7. Lined up in a straight row, this nose-to-tail traffic jam made up of some of the world’s largest ships would reach Fiji in the South Pacific Ocean from San Diego, California. And that’s just one year’s production. But where does this gigantic amount of steel go in the real world? Well, here are the top three uses:

Building and infrastructure (52% of global output, or about a billion tons annually): bridges, houses, railways, wind turbines, pipes etc.

Mechanical equipment (16%): pumps, cranes, compressors, heavy machinery, industrial equipment (reactors, boilers) etc.

Automotive (12%): cars and trucks

Interestingly ship building, together with locomotive and rolling stock manufacturing, takes up a mere 5% of all the steel produced worldwide, hence the lack of pontoon bridges to Fiji. Metal consumer products (cans, cabinets, tools etc.) on the other hand represent twice as much (or 10%) of global steel output.

But how is all that steel produced? First of all steel cannot be found anywhere in nature: it is a human creation made of carbon and iron. The former comes from the highest quality (coking) coal, while the latter (iron) comes from its natural ore (basically a form of “rust” found in large quantities.) The trick is, that after smelting iron (by heating it together with coal in a blast furnace), excess carbon has to be somehow removed, otherwise the result would be a rather brittle metal, useless in many applications. This step is done by blowing hot air through molten pig iron, in a Basic Oxygen Furnace and by adding some steel scraps. This classic blast furnace — basic oxygen furnace configuration is where 71% of global crude steel comes from; producing 2.33 tons of CO2 for every ton of steel made. (This is why the steel industry is accounting for 7–8% of all global emissions, alone… As usual, scale is everything.)

Electric Arc Furnaces, on the other hand, make steel mostly from scrap collected for recycling. Due to the relative low availability of scrap, compared to how much steel we actually need, this method caters for only 29% of global steel demand. In other words only one-third of all steel produced worldwide comes from recycling, while the remaining two-thirds still originates from virgin steel production described above. The reason is simple enough: steel produced in a given year lasts a very-very long time. Bridges, skyscrapers and infrastructure are usually built to last at least fifty years, and heavy machinery and cars also remain in use for decades. What we can recycle today was thus originally made 20–50 years ago, when 700–800 million tons were the total global annual output — a little more than a third of today’s production. So much for the scalability of low carbon intensity, recycled “green steel”…

There are two key takeaways here: one, most steel comes from coal burning blast furnaces and two, it is used in construction, cars and heavy machinery where it is locked up for decades, if not half a century or more.

And what do we see on the demand side? Global motor vehicle production still hasn’t climbed back to its 2017–2018 levels. The real estate bubble in China has burst for good with the bankruptcy of Evergrande and the bust of the whole business model it represented. The office space Armageddon is still not over in the US. Meanwhile Europe is de-industrializing fast, with car production, machine manufacturing and construction on the decline for three years now. In response to dropping demand worldwide crude steel production followed suit. (In fact, such metrics are a much better indicator of economic health than any fake GDP figure out there.)

The question poses itself: will there be a rebound anytime soon? Well, China is already well past its population peak, and based on fertility rates it is unlikely to resume growth anytime soon. And that means: there will be less and less demand for new housing; especially with a still relatively high youth unemployment and with a massive surplus of flats built already. (Many of them are still vacant as these housing units were bought for investment purposes and not for living.) Thus the question remains open whether the newest stimulus package manages to give a boost to other economic sectors. I’m a bit skeptical, but more on that later.

The US, on the other side of the Pacific, is drowning in debt already, with many banks teetering on the edge of bankruptcy. Meanwhile, the stock market bubble just keeps inflating, while the middle class gets impoverished and the only growth they see beyond the price of groceries is their credit card balance. Given these circumstances it shouldn’t come as a surprise that the Office CMBS delinquency rate spiked to a record 11%, blowing by the Financial Crisis peak… Not a sign of a coming real estate boom, let alone a consumer spending spree.

The 2025–2030 period looks even worse for Europe. With the recent announcement of (further) steel plant closures, wind farm projects cancelled and automotive companies laying off their workforce in droves due to a lack of demand, we will most likely see a further drop in EU crude steel output. Europe is already well past its peak annual steel production rate (the 2007–2008 period), and after shedding 40% of its crude steel output over the past one-and-a-half decade, it continues to march towards complete deindustrialization. (A half of that 40% drop occurred during the course of 2022 and 2023 alone — just sayin’.)

This brings us to the question of energy, the essence of every economic activity. Steel has a crucial role here: it is not only energy intensive to make, but also plays a critical role in energy extraction and conversion, too. Wind turbines sit atop massive steel towers weighing several hundred (and in some cases a thousand) tons, and now there are more than 400,000 of them worldwide. The weight of the steel casing in a single oil or gas well can also reach a hundred tons or more (depending on the depth of the well and the length of laterals)… And again, we are talking millions of wells here. As we can see, it takes a lot of energy (and materials) to get energy… And by the way the same goes to every other major energy source, including coal, natural gas, hydro etc. — all requiring steel to extract and build.

The problem is, as rich deposits of low-cost oil and gas slowly deplete, we will have to drill more and more wells just to keep oil production flat. Yes, there will always be inventions aimed at improving well performance, but the general trend is undeniable: newer wells are much less productive than older ones. The same goes to wind power or hydro for that matter: as the best locations become occupied, newer plants will have to be built in places where energy returns on investments are lower. So even as we drill and pipe more wells, or build more wind towers than ever, the energy produced per ton of steel invested will get lower and lower and lower… This means that more and more steel would be needed year after year to keep civilization humming along: to keep the increasing number of wells, wind turbines and other equipment built at a rate surpassing depletion, and to cater for our ever increasing energy demand. If we factor in that old infrastructure (bridges, tunnels, pipelines etc.) also need replacement over time, we really should be seeing an exponential rise in demand for steel products. At least in theory.

This makes the plateau of crude steel output all the more perplexing. If the world were indeed be moving away from fossil fuels — towards much more material intensive methods of generating electricity such as wind and solar — and if the world economy were still be growing, as suggested by GDP figures, we should be seeing a continuous rise in crude steel output. In an energy limited world, on the other hand, where less and less surplus energy is left after drilling (and piping) the next well, or building the next wind tower, (real) economic growth would be severely constrained. (Diminishing returns anyone?) As more and more steel output would be diverted to maintain the same level of energy output year after year, there would be simply not enough economic capacity left for replacing worn out bridges or to fix everything what is broken, let alone to increase vehicle production or the rate of construction. Meanwhile, the cost of building materials would be rising globally, preventing energy companies from continuing with drilling, building and piping… Just ask the folks tasked with drilling wells. Or how about looking at some numbers (emphasis mine):

“Growth in the oilfield service industry seems to be leveling off. After strong and steady growth in 2022 and 2023, the industry posted a more modest 2.4% increase last year and is forecast to shrink by 0.6% this year.” […] Moreover, a combination of wage inflation and rising material costs is putting pressure on EPC contractors and challenging their ability to maintain competitive pricing and secure new projects in a constrained supply chain environment. Trump’s return heralds a likely rise in protectionist measures, including higher US tariffs and tolls on imported goods. If the country imposes additional pressure on China with toll barriers in the range of 60% to 100%, the cost of essential equipment for energy projects could nearly double for developers that depend on China for supplies.

So, in light of all this, should we be surprised to see stagnant energy output, flatlining steel production and rising inflation, as we do today? I think not. Again, this was pretty much in the making for years now. According to an article published in the Journal of Petroleum Technology, “Energy necessary for the production of oil liquids is growing at an exponential rate, representing 15.5% of the energy production of oil liquids today and projected to reach a proportion equivalent to half of the gross energy output by 2050 (Delannoy et al. 2021). When the energy required for the extraction and production of these liquids is taken into account, the net-energy peak is expected to occur in 2025.” — that is, this year. Still surprised to see economic stagnation worldwide?

In a sense we see a rerun of the 1970’s oil shock. This time though it’s happening on a global scale… And just as back then, the reason remains a depletion induced increase in the energy demand of energy extraction:

“The decline in EROI among major fossil fuels suggests that in the race between technological advances and depletion, depletion is winning. Past attempts to rectify falling oil production i.e. the rapid increase of drilling after the 1970 peak in oil production and subsequent oil crises in the US only exacerbated the problem by lowering the net energy delivered from US oil production (Hall and Cleveland, 1981).”

Again, as production of the easy-to-get oil peaks in more and more places worldwide, no amount of drilling will be able to bring back the good old days. Chanting ‘Drill, baby, drill’ definitely will not cut it. Tariffs and wars, on the other hand, will only make it worse. And while the new US president invoking an ‘energy emergency’ — pushing federal land exploration, rare earth dominance, energy security, nuclear etc. —sounds promising, it simply will not be able to recreate cheap and easy to recover oil and other minerals. This policy, if pursued to its logical endpoint, will “only exacerbate the problem by lowering the net energy delivered” — be it from oil, nuclear or renewables. Every invention, every technological development to access hitherto inaccessible “uneconomic” resources has invariably pushed energy and material demand higher per unit of stuff recovered. And this is what makes the success of China’s stimulus package, too, highly questionable: while wording legislation and ceremoniously signing it costs next to nothing, it does not necessarily mean that the energy economics underpinning it all will work out just as fine.

Based on the data presented here, I argue, we are already knee deep into a major oil and energy crisis — much like the one overshadowing the 70’s and 80’s. This time though, there are no price hikes, no lines at the pump, no panic. Instead, we see stagnating economies failing to produce growth and unable to generate demand for both oil and steel. I might be wrong here, but if I’m right, this crisis of under-consumption and stagnation is here to stay for a few more years… At least until the continuously and exponentially (!) rising energy costs of extracting energy reaches a level where even cosmetic growth becomes impossible. No matter how much oil is said to be still in the ground, or how much more steel we could theoretically make. Once the energy cost of extracting/making them surpasses a certain level, it’s game over.

The past five years of stagnating steel demand, and a peak output in 2021, is but a symptom of a much larger global crisis in the making. The growing mismatch between the amount of energy and building materials needed to maintain our current living arrangements — let alone real economic growth — has profound effects all across the globe already. Falling birth rates, inflation, rising debt levels, soaring economic inequality, trade wars, the return of great power politics are all symptoms of a civilization passing diminishing returns on multiple fronts, all at once. It’s not that the world economy will topple over tomorrow due to a lack of resources and energy. We still have a lot of stuff left, but the growth-enabling, low-cost, easy-to-get half is now gone. The remaining half will be increasingly hard to get: it will require more work, more investment, more energy, more materials… Yet, extracting them will provide lower and lower rewards and produce more and more inequality and conflict. The end of growth is here, and it’s going to be increasingly messy.

Until next time,

B

The Honest Sorcerer is a reader-supported publication. Please consider a subscription or perhaps buying a virtual coffee… Thanks in advance!

Peak oil, peak steel, peak democracy, have we reached peak hubris yet? Or are humans gonna keep on keeping on until there's only peak radioactive charcoal to defend?

An excellent article yet again.

Too many humans, using too many natural resources, and producing too much pollution, including heat and GHGs. Last one out, turn off the lights.