Don't Look Up!

What previous oil crises can teach us about this one, and what to expect in 2027 and beyond

{kind=link}

I have to say, I’m terribly frustrated. Everyone admits that what we are going through is the biggest energy crisis in history, yet western governments, the media and heads of corporations act as if nothing’s happening. An enormous ball of dung is hurtling towards us, yet all we are told is just to keep on working, commuting, shopping and feeding our retirement savings into the biggest stock market bubble in human history. Yes, it smells bad, looks bad and now blocks out the Sun, but hey, we must beat the Chinese competition and increase our profitability at the same time! Work harder and accept less! The cognitive dissonance could not be harsher.

And when the crisis do gets a passing mention, it’s treated as a temporary phenomenon. Something, which will eventually (think: within a couple of months) sort itself out: the strait will be open soon, ships will return by summer, and oil will flow just like before in autumn. If you’ve read my earlier posts on the topic, you know that ain’t so. We are on track to lose 2-4 billion barrels of oil, or 6-12% of global crude and condensate production by the end of this year. No reserve or oil storage is big enough to compensate for that—someone will have to eat the losses. That is the ball of manure, which is getting larger and larger with every passing day. And it’s not just crude oil, but fertilizer, sulfuric acid, jet and diesel fuel, naphtha, helium, aluminum, LNG—everything this bloody civilization needs for its survival. Combined with record setting ocean temperatures (even before the super El Nino arrives later this summer), massive droughts in North America and Europe, this crisis is shaping up to be the biggest humanitarian crisis in modern history as well. But hey, profitability is falling, so get back to work and keep on shopping! Don’t look up just keep on burning that fuel, as if there’s no tomorrow. Well, with that mentality, there will be no tomorrow, that’s for sure.

Now, with that said, let’s see what are the lessons to be learned from previous oil shocks. What to expect in 2027 and beyond? Will there be a return to previous flows, even if equipment takes months to repair? How will the world look like years after hostilities in the Strait of Hormuz end? These were the questions I was seeking the answer for as I dug deep into the EIA archives. Some of the answers were obvious, but some were a surprise… So without further ado, here is what I found.

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

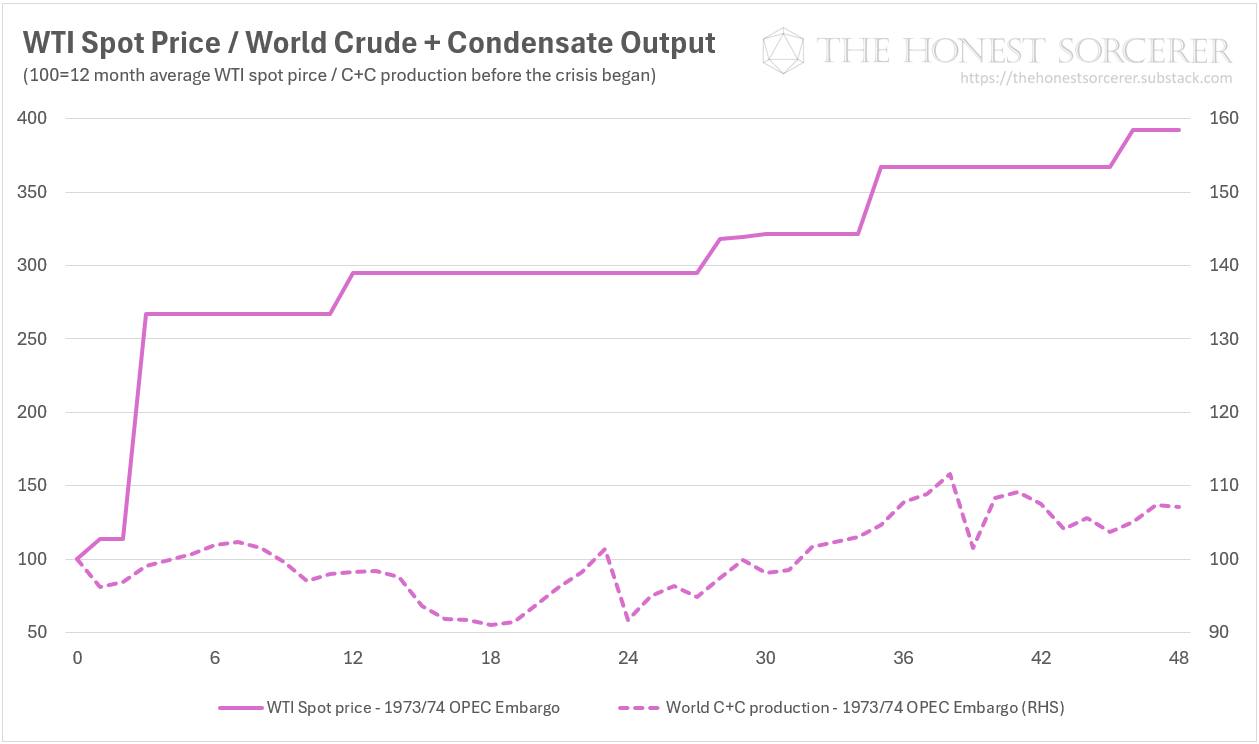

1973/74 OPEC oil embargo

First, let’s see what were the major oil shocks in history, and what their impact were on global crude oil (plus condensate) output. The number one, which comes into everyone’s mind, of course, is the 1973/74 OPEC oil embargo. Launched by the Arab members of the Organization of the Petroleum Exporting Countries (as part of their ongoing war against Israel’s expansion) in October 1973, it became the pivotal geopolitical and economic crisis of its time. While it lasted only five months, till March 1974, it ended up quadrupling oil prices and causing severe gasoline shortages all across America and Europe. And these effects haven’t faded away with the crisis ending: oil prices remained elevated, sparking a global wave of inflation and kick-starting the de-industrialization of the West. It marked the transition from the post-World War II "golden era" of manufacturing prosperity to a phase of decline, where older industrial regions—particularly in the American Midwest and Northeast—began experiencing significant factory shutdowns and disinvestment.

US conventional oil production also continued its long decline (after peaking in 1970), but new entrants to the world market managed to offset the fall in US output. The 1973/74 oil crisis was thus not due to a lack of oil in absolute terms, but was caused by a selective embargo imposed on Western countries. The economic fallout from the event and the ensuing demand destruction, however, have resulted in suppressed oil demand for years to come. It took a full 32 months (from the start of the embargo) till world crude plus condensate production returned to a growth trajectory, surpassing pre-crisis levels for a sustained period of time. The chart below speaks for itself:

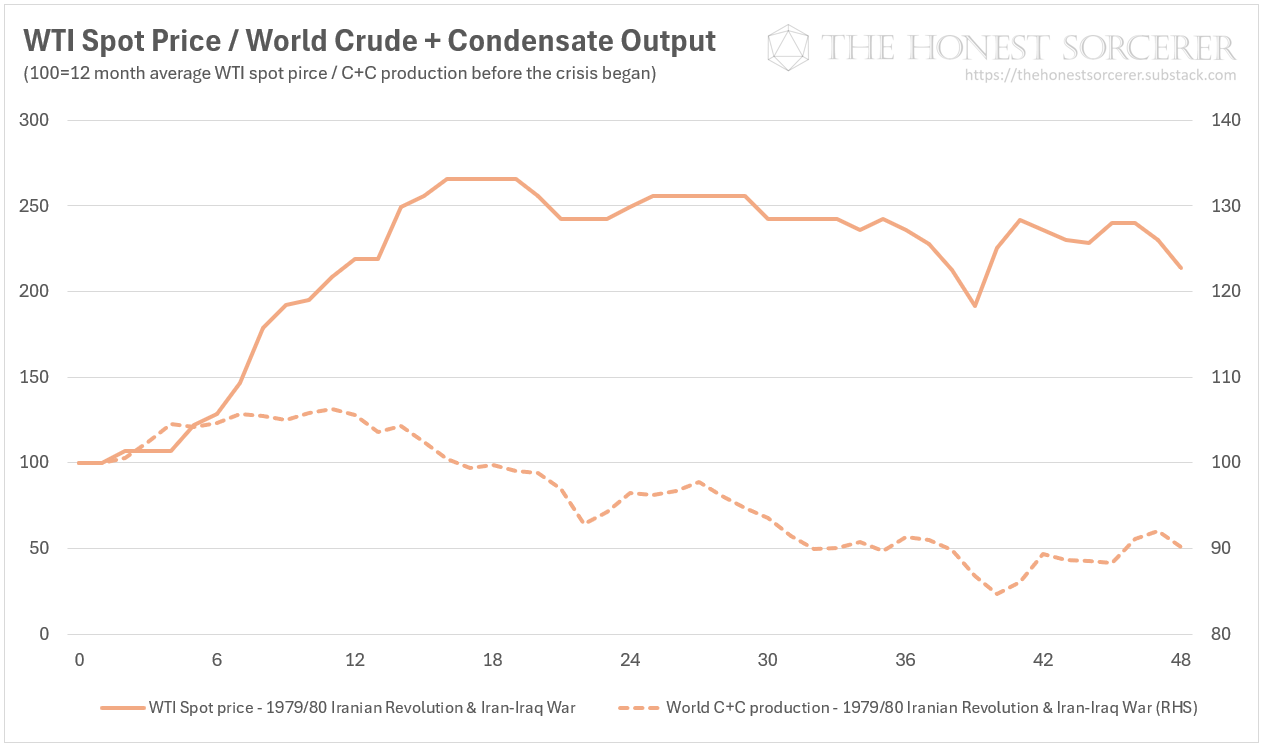

1979/80 Iranian Revolution and the Iran-Iraq War

Just four and a half years after the previous crisis ended came a second shock to the system. Amidst a popular uprising against the dictatorial rule of Reza Shah Pahlavi (imposed on the Iranians by a western orchestrated coup1) oil workers went on a strike, lowering Iran’s oil output from 6 million barrels a day in September, 1978 to 0.7 in January, 1979 (the starting point of our chart below). These news, invoking fears of another round of shortages, have led to widespread panic buying and hoarding of oil—despite the fact that production was restored relatively quickly and world crude output was on a track to surpass 1978 levels by a comfortable margin.

This behavior—combined with an economic rebound from the ill effects of the 73/74 oil embargo—still led to a price rally nevertheless, raising the cost of a barrel by 166% in little more than a year. Then, in September 1980, Saddam’s Iraq attacked Iran’s Islamic Republic, with the full intelligence and weapons support of Western countries. The war has led to a collapse of both nations’ oil production, reducing their combined (and already declining) output by 5 million barrels a day (see the trough at month 22 of the crisis on the chart below).

Oil prices barely nudged, though. In fact, they began to fall, then stagnate. The economic crisis started by the energy price rally in 1979, have already made its effects felt—together with the energy saving measures introduced in response to the previous oil shock. Demand was falling as Western nations continued to outsource energy intensive production to China (and elsewhere), fuel economic vehicle sales rose and as the G7 economies were entering a double dip recession and a period of stagflation. OPEC nations began to cut their oil output to stabilize prices, but all they managed to achieve was lowering global crude oil output for many years to come. Central banks raised interest rates to stratospheric levels, investment plummeted, and neoliberal policies (outsourcing, financialization, privatization) ruled the day. It wasn’t until August, 1989—ten years and eight months after the crisis started—when world crude oil output managed to rise back to 1978 levels in a debt fueled economic boom. The second oil shock took a full decade to recover from.

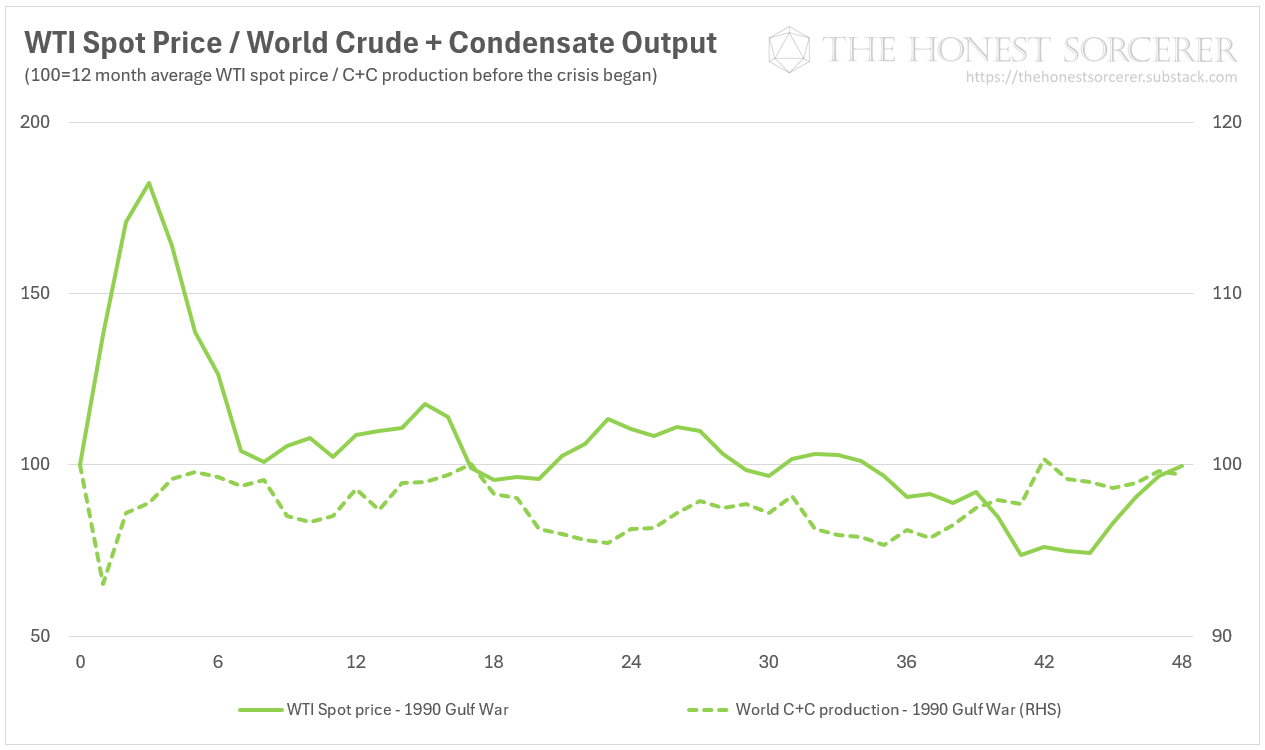

1990 Gulf War

Just as the economy was recovering from the deep recession of the early 1980’s, and as the Soviet block was in the process of disintegration—signaling the “end of history” and the “victory” of capitalism over communism—came a third shock. This time, Saddam’s Iraq was invading its smaller neighbor: Kuwait. The West’s response was quick and decisive: Desert Storm destroyed Iraq’s military, and a UN embargo on Iraqi and Kuwaiti exports, imposed in August 1990, destroyed Iraq’s economy. Oil prices shot up (briefly), but crude oil output failed to return to 1989/90 levels for four years to come.

The economic collapse of Russia and the Eastern European block—together with the continued deindustrialization of Europe—also played a role here. So while the economy of the West suffered “only” a year long economic recession in 1990, Eastern Europe has entered a prolonged period of immense economic hardship following the collapse of its markets and trading system.

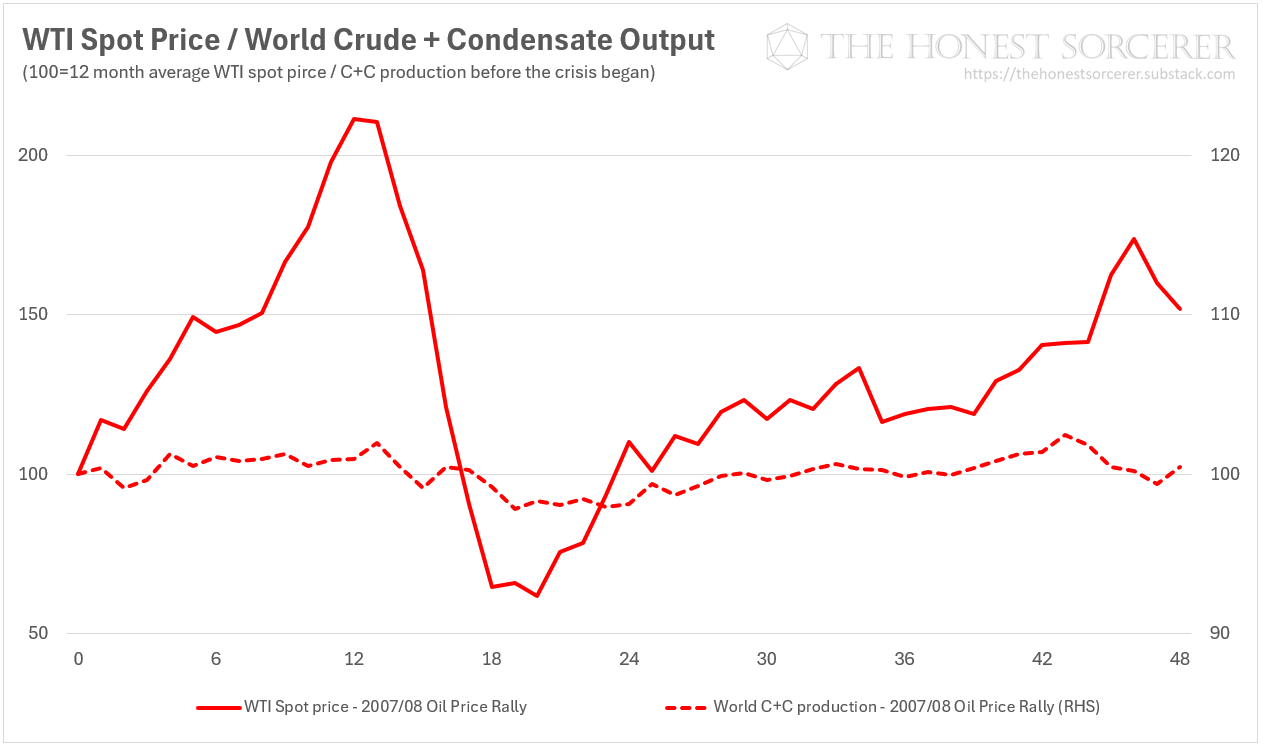

2007/8 Oil Price Rally

Now, this is a strange one—at least for the casual observer. Chinese and Indian oil demand kept rising fast, Europe’s economy was finally recovering, world trade was booming—what’s not to like in that? The demand for oil, moving, mining, feeding and building an ever larger world economy was on the rise, too—but supply was stagnating. The reason: world conventional crude and condensate production has peaked in 2005—as predicted—and unconventional sources (shale, tar sands etc.) haven’t come online yet.

This irreconcilable mismatch between supply and demand has led to a worldwide price rally, with spot prices briefly touching $146 in July 2008 ($200 in today’s money). The spike didn’t last long, though. The great financial crisis of 2008/09, following the collapse of the housing market, left every business scrambling for cash; triggering a massive sell-off of everything: from physical commodities to mortgage backed securities. Oil prices collapsed within a matter of months—together with world trade and the demand for oil.

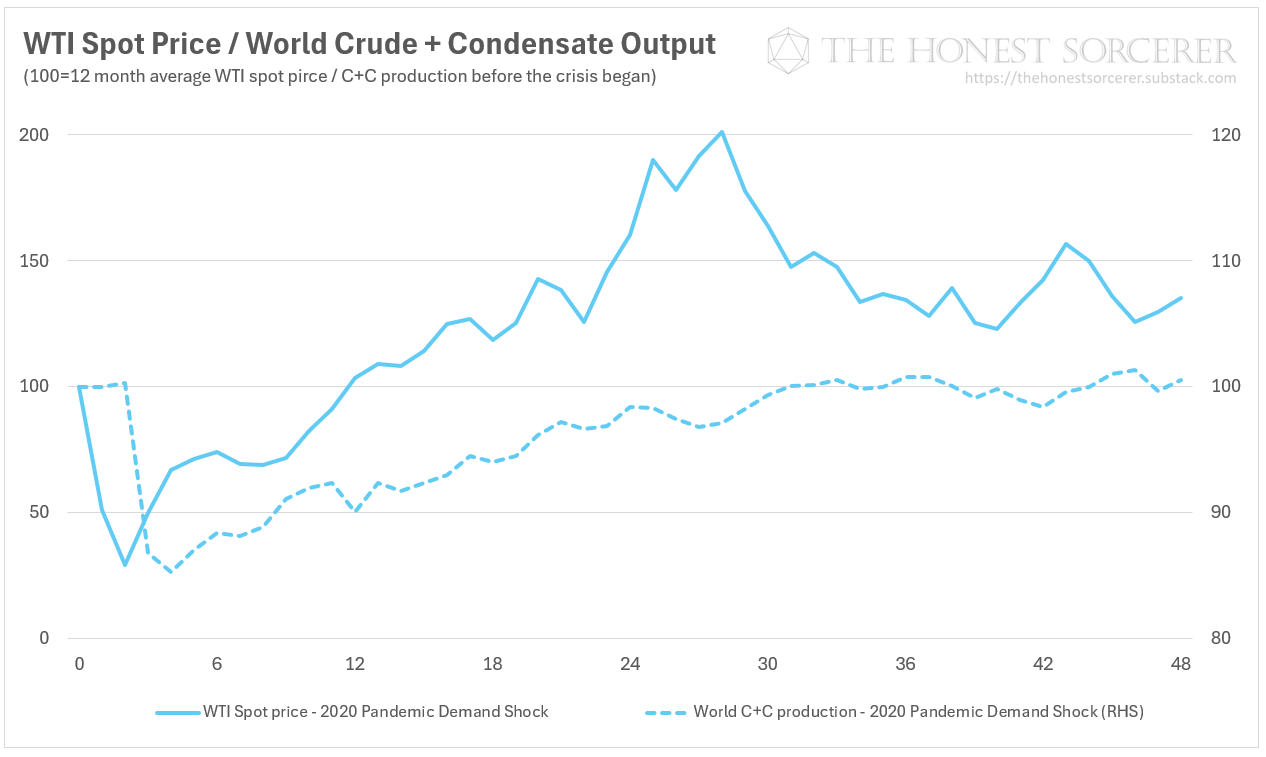

2020 Pandemic Demand Shock (plus Russia/Ukraine)

After the rather anemic growth of the 2010’s, hallmarked by zero interest rate policies and high (then collapsing) oil prices, 2020 saw the entire world economy grind to a halt. In response to the rapid spread of COVID-19, most countries around the world entered a lock-down, leading to a sudden drop in oil demand and seeing prices reaching negative levels for a brief period of time. 13% of world crude oil production was shut-in during April and May, then gradually began to recover as economic activity slowly returned.

The demand crisis then quickly turned into a lack of supply predicament in 2021. Despite oil prices recovering to pre-COVID levels in a year, oil production was still 8% lower than in 2019. This mismatch, fueled by a quick economic rebound and a slower than expected return of supply, saw prices surging 40% above pre-pandemic levels by late 2021. Then came Russia’s invasion of Ukraine, and the fear of western sanctions completely crippling Russian oil exports. Prices doubled compered to 2019 levels, even as the worst fears of the market failed to materialize and as world oil production kept recovering. As the war premium slowly faded away, following a hitherto unprecedented release from US strategic petroleum reserves in two waves, and as oil supply returned to pre-COVID levels two and a half years after the lock downs began, prices finally stabilized.

What’s in common?

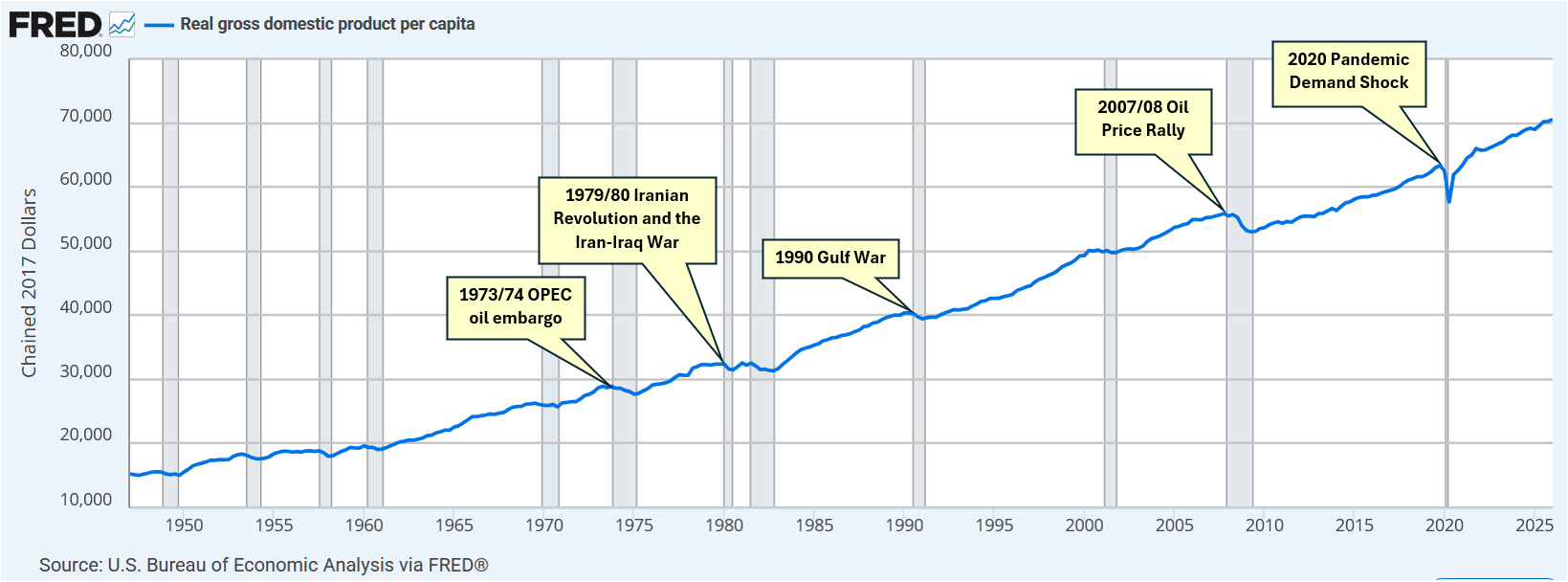

The first pattern we can easily identify by looking at inflation adjusted per capita GDP figures (here showing the results for the world’s largest economy), is that oil crises are followed by a recession. Four out of five times. The last time oil prices doubled compared to pre-crisis levels (during the early months of the war in Ukraine), US inflation adjusted per capita GDP kept growing, but only at the cost of Europe further deindustrializing itself, the US budget going into deep deficit, and credit (both private and public) shooting through the roof.

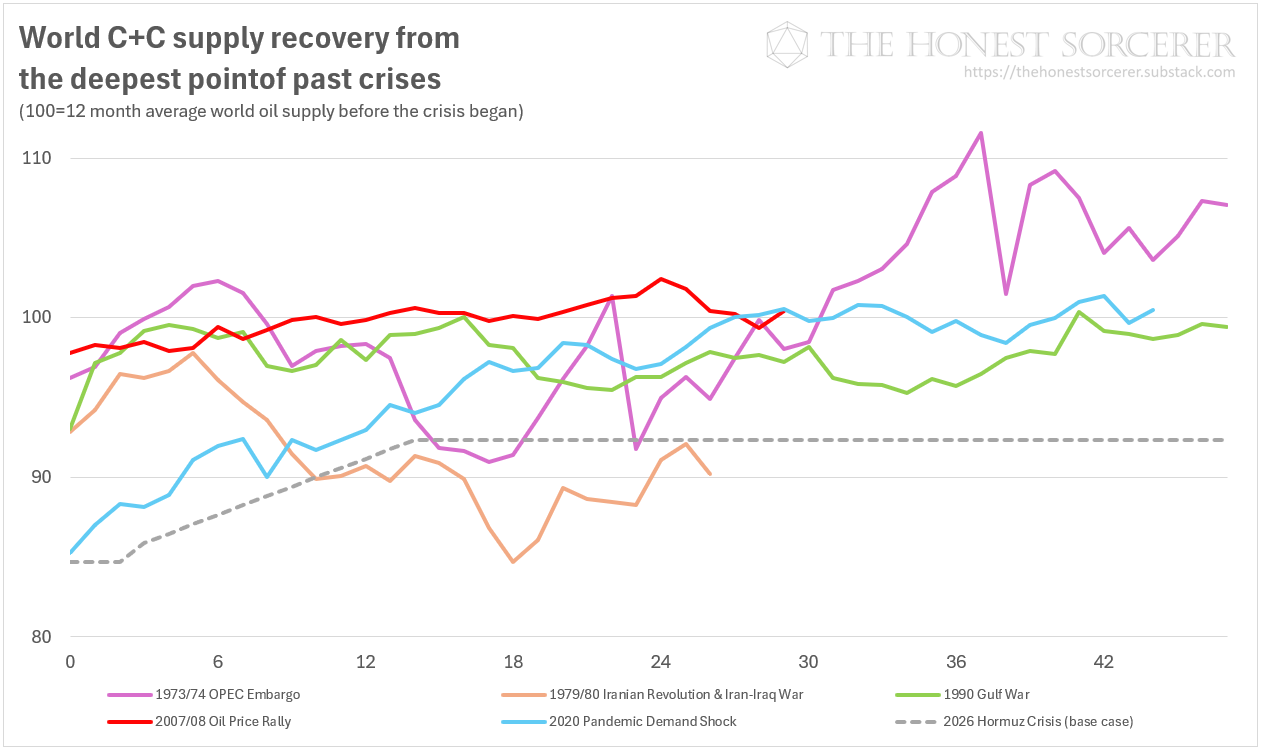

Now, that we are facing by far the biggest oil supply shock in human history, threatening the entire world economy with a very long recession (if not economic depression), the United States won’t be spared either. As for an illustration how the Hormuz blockade compares to previous crises in the past, and what to expect in terms of recovery, take a glance at the chart below:

While previous supply crises saw oil production drop 2-7 percentage points, this one took out 15% of global crude supply in one fell swoop. And the end is nowhere in sight. As of the time of this writing, the Mexican standoff between Iran and the US still holds, even as American consumers and airlines are hitting a breaking point. The demand destruction, which has ensued from each prior oil crises, can expected to be especially severe in this case. While the past certainly does not repeat itself, it took several years, if not a decade for oil production to recover from previous troughs. If there is any historical analogue (in terms of magnitude at least) to the present crisis it lies closest to the Pandemic shut-in, or the deep recession following the Iranian Revolution and the Iran Iraq war in the 1980’s. Neither suggests a quick recovery on the other end. The deeper the Hormuz crisis goes, the longer and more questionable the recovery will be.

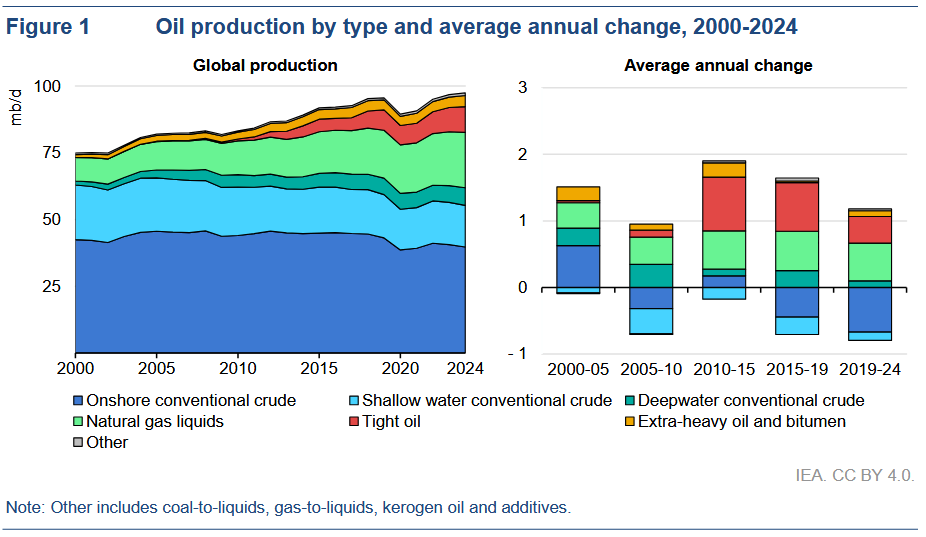

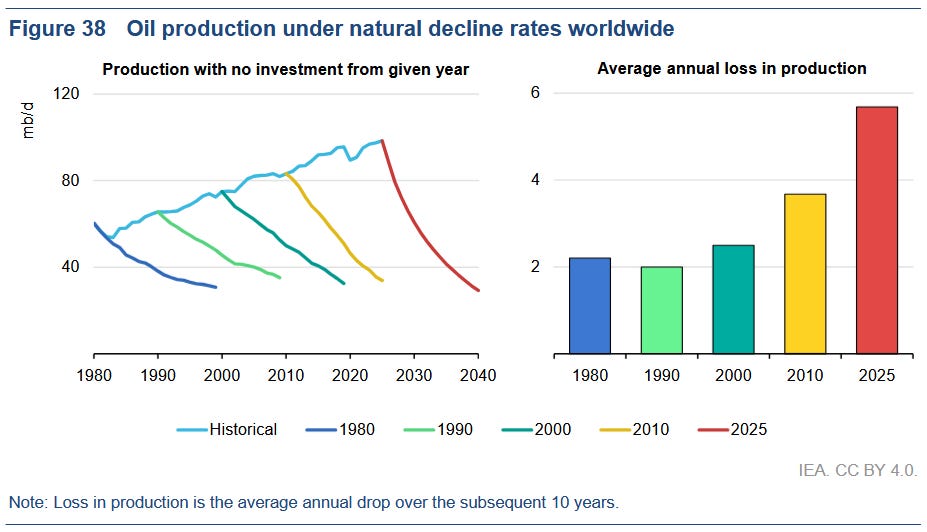

And this is where the IEA study I wrote about last year comes into sharp focus again. We are rapidly approaching the point in world crude oil production where the ever accelerating decline of older plays eventually outpaces the production from newer ones—even without geopolitical turbulence. And with less and less new oil to be found, much of global supply now comes from legacy and post-peak fields.

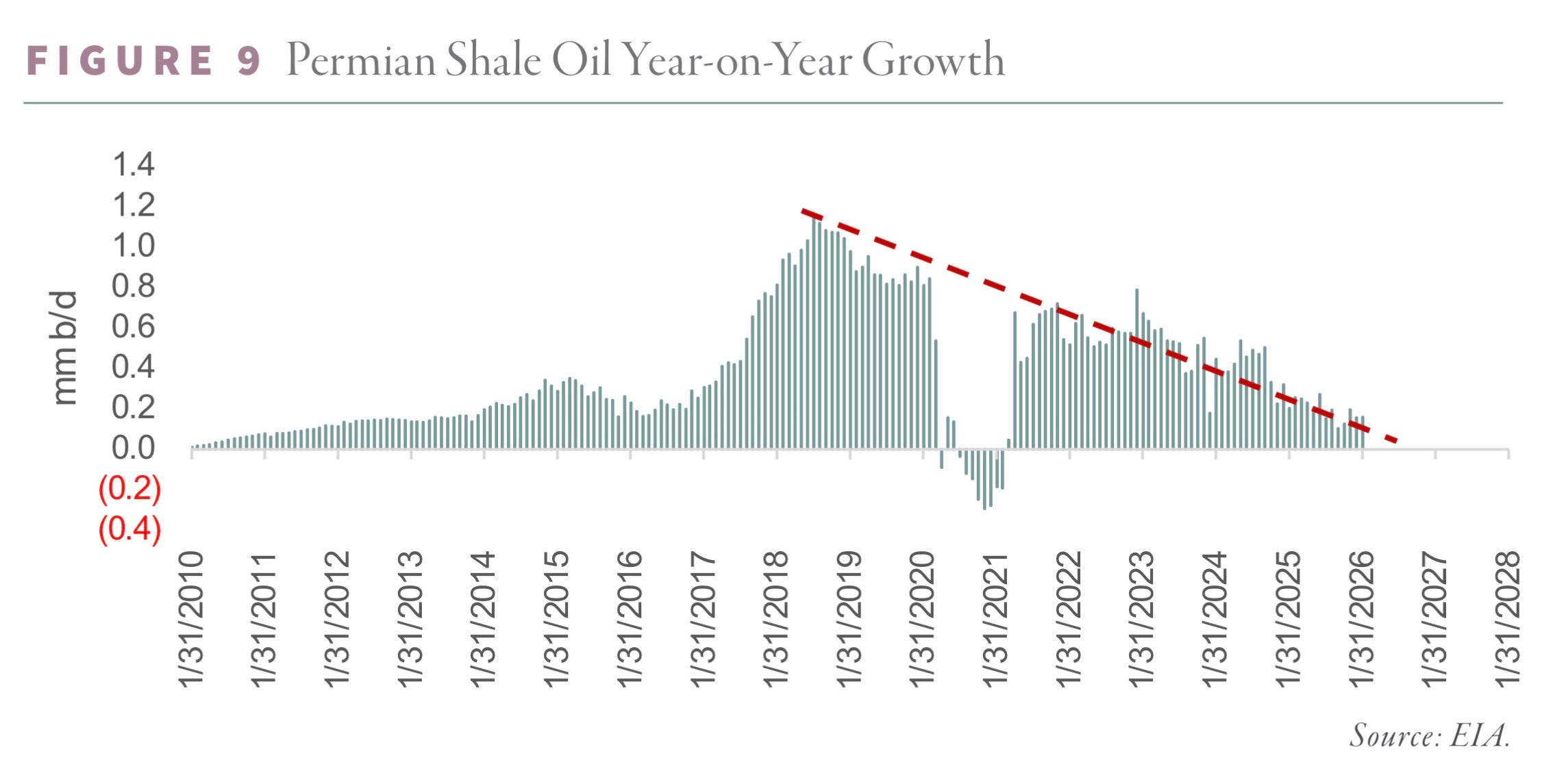

So while high oil prices can incentivize new drilling—$100 oil could unlock 2.1 million bpd of additional South American crude supply, according to Rystad—this will be nowhere near enough to compensate for the loss of 11-13 million barrels from the Persian Gulf. There is very little, if any, production to be ramped up elsewhere on the planet. In America, the world’s largest shale play, the Permian, which was single-handedly responsible for much of the production growth after the pandemic, is also facing exactly the same predicament. It was getting harder and harder to increase production already, to the point where in late 2025 shale growth has entered it’s own long decline. And while higher prices could provide one final boost, the EIA forecasts US oil production to peak by 2027 no matter what.

What this means for future oil production is not terribly hard to guess. With the shut-in of the majority of Gulf oil production we’ve just got a lot closer to the point where global oil production tips into a permanent decline. In fact, it’s quite possible that February 2026 marked the highest point in world crude oil output. Ever. And while it is certainly possible to build pipelines, such as the newly announced Basra-Haditha oil pipeline, avoiding transit through the Strait of Hormuz, it takes years and multiple billions of dollars to build out the necessary pipeline system. It’s much easier to pay a transit fee.

Conclusion

The situation around the Strait of Hormuz is shaping up to be a decade(s) long crisis leaving everyone affected. Based on the analysis of past oil shocks, recovery of oil supply could take years to a decade, further hampered by economic decline. Based on the size of the present supply outage—which is at least twice as large as any other supply crisis in the past—a major economic downturn worldwide is all but guaranteed, with a fat tail risk of this crisis turning into an outright economic depression lasting many years. Consequently I find the return to February 2026 world crude production levels highly unlikely before 2028—if ever.

Based on this analysis high oil prices will eventually break the economy, and thus will not—and cannot be—sustained. Demand for oil is already in the process of being destroyed, and is unlikely to return during a prolonged period of economic hardship—further delaying the recovery of oil production. Since many oil fields affected by the blockade of shipping was already ageing, such a prolonged shut-in of production could damage these fields beyond repair, preventing their reactivation. So while a partial recovery is certainly possible once a solution is found to the geopolitical crisis at hand, the longer this stalemate holds, the lower that rebound in production will be. And the longer we have to wait for a political solution, the more likely accelerating decline from legacy and post-peak oil production elsewhere will arrive, putting a definitive date on the peak of the carbon pulse.

Until next time,

B

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

“In 1953, amid a power struggle between Mohammed Reza Shah and Prime Minister Mohammad Mosaddegh, the U.S. Central Intelligence Agency (CIA) and the U.K. Secret Intelligence Service (MI6) orchestrated a coup against Mosaddegh’s government. Years later, Mohammad Reza Shah dismissed the parliament and launched the White Revolution—an aggressive modernization program that upended the wealth and influence of landowners and clerics, disrupted rural economies, led to rapid urbanization and Westernization, and prompted concerns over democracy and human rights.”—Source: Britannica

Spot on. The decline in EROEI doesn't just lead to a "simplified" society; it triggers what we might call Systemic Cannibalism.

When a complex system can no longer pay its "complexity tax" with new energy flows, it stops growing and starts eating itself. We are seeing this play out in real-time: institutions, social classes, and nations are no longer cooperating to expand the pie, but are actively fighting to liquidate each other’s assets to maintain local stability.

Well done, a very plausible analysis. It had to come some time, but 2026 looks like peak oil. We can only hope it augurs a rapid collapse of industrialism and a rapid decline in carbon emissions.

What's amazing to me is that stock markets have yet to react to the near certainty of global economic recession. They say that markets are "forward looking", but right now they seem to be blind. A perfect example of being "energy blind".