The Big Picture

On why having a plan does not equal having a well-thought-out plan

The time has come for one of those broad view “in the grand scheme of things” type of articles on energy, resources and geopolitics. And while my experiments to develop an all-seeing crystal ball haven’t yielded any result yet (trust me, it’s just another six years away!) I think what we have learned so far can still help us to put current events into a bit more context than what meets the casual observer’s eye. How does changes in energy use explain who is in power? How could a nation consuming 16% of world energy production while constituting only 4% of it’s population dominate the entire planet? Can switching into electricity change that picture?

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

Power is key

Let’s start with one of the basic laws governing life: energy is (almost) everything. Without energy, there is no movement, no light, no heat, no change—just the opposite: cold, darkness and slow decomposition. In other words: a steady and relentless rise in entropy, or disorderliness. What’s even more important than energy is its flow—power—the rate at which work is done or energy is transferred. This is the amount of heat, electricity, light, movement, physical or chemical change generated or done in a unit of time—a second, an hour, a year. Contrary what your local priest of economics tries to tell you, this is what really matters—GDP, inflation and all the rest comes only thereafter.

Throughout 99.3% of human history the rate of technological, societal or economic change was limited by the amount of energy we could capture from the Sun in any given year. Think: plants collecting sunlight and turning it into edible energy (food). Gusts of wind and the flow of rivers moving ships and mills—making us entirely dependent on the weather, which too was ultimately powered by the heat emanating from our central star. Much of our history revolved around how to capture even more of our Sun’s power and how to turn it into more humans and more affluence for those who ruled over us. As hunter-gatherers we kept expanding our reach till the entire planet became ‘our’ hunting ground from the Arctic Ocean to the southernmost tip of the Americas, Africa and Tasmania. Then came agriculture, an even more intensive method of harvesting sunlight, using high-calorie seed plants (wheat, barley, rice, corn, legumes etc.). It was no coincidence that those kings had the most “power” who controlled the most of the energy harvested—either through direct taxation, colonization, or by controlling trade. And the higher the surplus was, the wealthier their kingdoms became.

Towards the end of the 18th century, in our relentless search for more power, we found a way to harness the power of conserved sunlight: fossil fuels. Long dead plants—buried deep underground in the form of coal, oil and natural gas—stored way more concentrated energy, than even the best firewood or the best crop could ever provide. Work was no longer limited by the amount of calories available, or the ability of humans and their animal slaves to convert food into work. Instead we got hold of a seemingly unstoppable 24/7 flow of high grade energy, which our machines, locomotives, ships, then later power plants trucks and planes converted into more products, food, raw materials, transport, trade or what have you. Our rate of energy consumption—a.k.a. power—shoot through the roof, together with the political power of a wealthy elite who controlled it all. Together with technological change political change has also got accelerated: producing not one but two world wars, the rise and fall of communism, a series of boom and bust cycles and so on—all within a span of a century.

There is a reason why I wrote at the beginning of this essay that energy is almost everything. The other thing to keep in mind is matter. See, you can have all the power at your fingertips and still perish. Think of being stuck on a newly formed volcanic island in the middle of the Pacific Ocean, receiving plenty of tropical sunlight and producing a steady flow of high grade geothermal heat. If, however, you have no material resources you are still screwed. Without metals—and a range of other materials (such as wood), let alone croplands or fresh water—you’re basically sentenced to death. Even if you had a favorable climate on this island with rivers and a fertile topsoil but no minerals, metal ores or fossil fuels (just plain volcanic rock), you still couldn’t build technology and tools required to harness geothermal heat and solar power beyond any level seen during medieval times. Sorry, no fossil fuels, no metals. No metallurgy, no electricity. And without electricity there is no modernity either, just wooden shacks, sheep and horses.

Now, you see, the problem with mineral wealth—just as with energy—is that access to it is unevenly distributed. Some places have highly concentrated copper ore, others have high quality crude oil, yet others can produce prodigious amounts of food crops. Hence the need for global trade—which was and to a large extent still is—the best practice to maximize wealth and prosperity. There is a major, completely—and dare I see deliberately1—overlooked, issue here. Namely, that none of these resources are infinite. In fact, highly concentrated ores, easy-to-get conventional oil etc. are finite and very-very slow to renew. There is a good reason we call them non-renewable resources. Once you draw these down, you will have to wait eons for geological and ecological processes to regenerate them.

This doesn’t mean that we’re running out of copper, oil or coal anytime soon: we are “just” running out of their easy to access, close to surface, highest grade portions. The rest—which actually constitutes most of these resources—are increasingly harder to get, take more energy, raw materials, work and ever more sophisticated machines to obtain. Problem is that beyond a certain point the economics of extracting these resources simply stops working; not everywhere, all at once but in more and more places. Mines close because all the high grade (high metal content) ore is gone, and not because there is nothing left. What remains would just take too much explosives and diesel fuel to dig up and an increasing amount of electricity, fresh water and chemicals to process (crush then extract). Oil fields, from where oil used to be gushing out, now require pumping water and chemicals underground to force what can be still extracted to the surface.

The energy cost of extracting resources goes up in a slow but exponential fashion over time. The thing to note here is not the exact technique used to get a certain resource (be it fracking, or various secondary and tertiary recovery technologies) but the slow and ever worsening trend. Simply put: as it takes more and more energy and other resources to get the same amount of coal, oil, copper etc. year after year, more and more of the said resources will have to be returned into extraction—leaving less and less surplus for the economy to work with. This is how technological innovation, enabling the extraction of hitherto inaccessible resources, turns into a trap: requiring us to run ever faster just to stay in place.

As our efforts to get the next batch of resources require more and more complexity and hit diminishing returns, the economics of extraction and production begins to break down. Again, not everywhere, all at once—but one place after another. These small changes do add up, however, and we eventually get to the stage where the global material economy simply stops growing. See, for example, the case of copper and silver, two highly sought after and essential inputs to all things high-tech and electric from solar panels to microchips and data centers. Silver is already past its production peak, and copper is expected to reach it before 2030. (If it haven’t hit it already due to the Hormuz crisis limiting sulfur exports—a key input to processing certain copper ore types.) Those who are actually working in these high tech industries—and not just reading articles about how Tesla replaced copper with aluminum in low voltage systems—know what this means. In short: nothing good. And the same goes to crude oil as well, although the timing is more uncertain as geopolitics play a increasingly bigger role.2

When viewed from a global growth perspective, recycling mathematically cannot help to restore material growth either. Since a certain portion of the material is always lost in the process, a “circular economy” can only slow the decline somewhat—neither stop nor reverse it. Once mining of a certain raw material peaks then begins to decline as depletion accelerates, global usage of that substance begins to fall, too. Needless to say, but equally importantly, you cannot recycle fossil fuels which are still absolutely essential in every step of the large scale production of “renewables”, nuclear power plants, space rockets, plastics, fertilizer—not to mention mining, agriculture, construction and long distance transport.

The extraction of energy and raw materials, and the rate of which these are spent, defines economic and political power. High energy throughput → high GDP → high political (and often military) power. Money is just an intermediary in the process, facilitating trade but ultimately having no intrinsic value of its own. This is why Luxembourg—a tiny country in Europe with a ginormous GDP per capita—is not a world superpower: it merely handles other people’s money, but produces and processes very little raw materials and energy of its own. Exactly this is why the United States, still consuming 16% of world energy (despite having only 4% of global population), is a world superpower—with a ton of caveats, of course.

And this is why America sees China—a country using almost twice as much energy and housing four times as much people—as a major threat. And while we can debate how GDP is counted, whether based on purchasing power parity or in nominal terms, judging by its energy and raw material consumption calling China “the second largest economy” of the world simply doesn’t stand to reason. Especially so, if you consider how advanced and efficient Chinese manufacturing is, and how much high-tech they produce from electric vehicles to rockets. Holding on to a status quo, where the United States maintains its global economic and military dominance with only a half as large economy as the next country in line, thus not only generates friction but comes with a grave risk to the entire world—US citizens included.

Will there be a next world hegemon?

The world economy was already running close to its maximum level of power and material output—even before the events of 28 February, 2026. And that goes equally to fossil fuels and the metals needed to build an “electrostate.” See, despite “renewables” gaining a huge ground in electricity production and the immense efforts China made towards electrifying its economy, the world has already been running out of growth-enabling, low-cost resources… And with the onset of the long emergency started by the closure of Hormuz global material growth will not likely to return to previous levels any time soon.

It is also worth noting that electricity is an auxiliary power source—not a primary source of energy but something generated at a loss and by using tremendous amounts of mineral inputs.3 Sure, in many applications (cars, trains, city transport and short range logistics) electric vehicles can offer an alternative, and “renewables” can be a useful addition to support households (especially in poor regions, where the grid is nowhere near as well developed as in the West or in East Asia). With that said, these solutions are still a mere extension of the fossil fuel based energy system, not a complete replacement to it. So, while what can be electrified will be electrified—it will be done only to the extent of technological capabilities and economic return on investment, or as long as cheap raw material and energy supplies last. See, there is only so much the world can do before it runs low on fossil fuels needed to mine, smelt and manufacture metal parts, or it depletes rich metal ore deposits to a point where continuing extraction becomes uneconomic—whenever that arrives. Simply put: economic growth cannot be maintained by switching to “renewables”—especially not in a world which can no longer produce more copper, silver and a range of other materials needed to make the switch. In other words: there is no next economy.

China’s growth model is just as flawed as that of the United States’. It is materially impossible to keep an economy growing forever on a finite planet—and it really doesn’t matter if you run a petrostate or an electrostate.

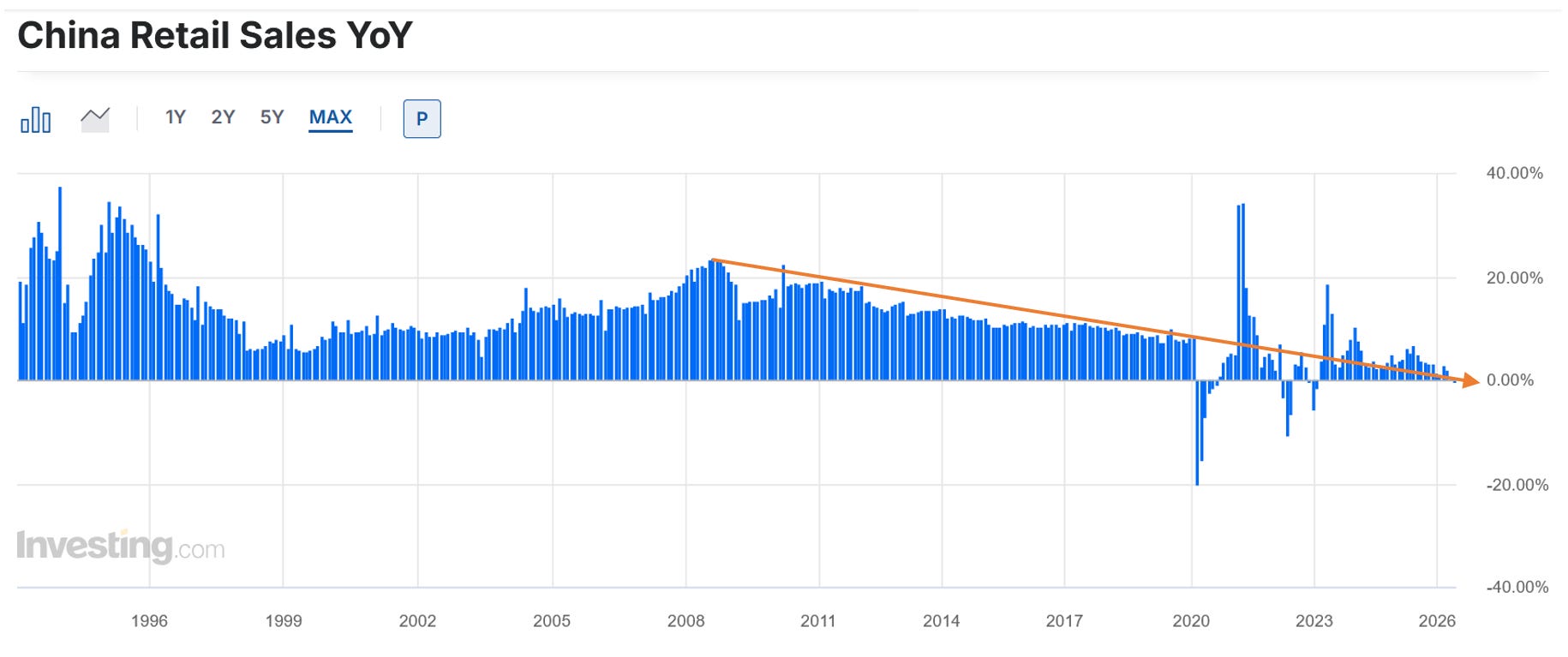

The world, near the definitive end of material growth, thus finds itself in a zero- then negative-sum game. In a global economy, where less and less is produced, mined, manufactured, there will be lower and lower need for services, insurance, banking etc.—not to mention the issue of our debt based money system requiring eternal economic expansion to avoid collapse. This is why Chinese retail sales growth turning minus 0.6% year-on-year is a huge development. This is not an outlier, but a continuation of a decades long trend which started in 2009, marking the peak of Chinese household spending growth. (This is exactly what I warned about two weeks ago.) In May alone, EV sales in China fell by 9% and overall car sales declined by a sizable 22.3%. China’s solar boom is also slowing down. Chinese customers are not switching to electric, they’re hunkering down. Bad consumer loans from credit cards to mortgages have been already surging over the past few years, with 10.6% of Chinese adult population falling behind on debt payments. Non-performing household debt soared 21% last year to a record of 2.2 trillion yuan ($329 billion), undermining all government efforts to boost spending. And while growth in exports managed to keep Chinese GDP growing, shrinking fixed asset investment (money spent on building more factories, buying more equipment etc.) indicate a coming end to export growth as well in the years ahead.

China is no longer a booming economy—quite the opposite—and the US economy is not in a much better shape either. Let’s face it: the world cannot afford more consumption, neither from a resource, nor from a consumer side—let alone from an ecological perspective. What we are thus seeing is a competition between a now rapidly fading hegemony—which together with its allies used to dominate more than 50% of the world economy after World War II—and a peaking then soon to be declining mega-economy, burdened with non-performing loans, a collapsed housing market, a lack of internal demand growth and a shrinking (albeit still huge) population. A decline in energy throughput favors dissolution and simplification—not an increase in complexity and power.

The long shadow

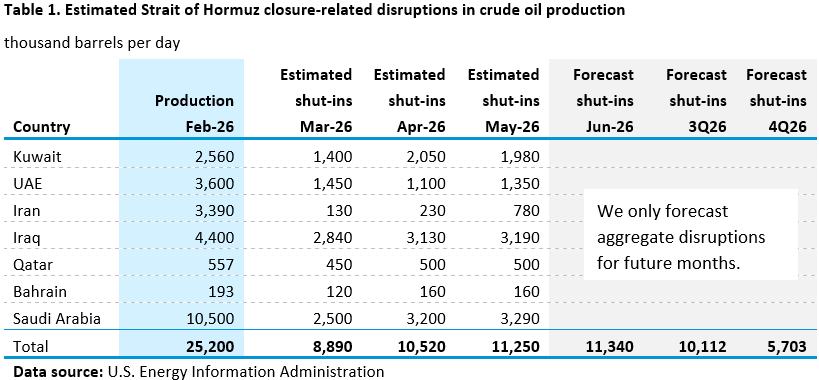

Understanding how energy, and especially oil, underpins the world economy, helps us to put the current crisis in the Middle East into a proper perspective. Choking off 13% of monthly world crude oil supply has caused an unprecedented shock to the world economic system. So far more than 1 billion barrels of oil was not produced, not delivered and not refined into products. Un-sanctioned Russian and Iranian shipments, leakers from the Persian Gulf, oil from floating storage, demand destruction in South and South East Asia, as well as local and strategic petroleum reserve draw downs (primarily in the US and Japan) helped to fill in that hole—at least partially but never fully. The US Strategic Petroleum Reserve (SPR) has fallen to 331.2 million barrels, the lowest since 1983. Global on-shore inventories are already at record seasonal lows, and the end of the crisis is still not in sight. Depending on how fast and to what extent oil production in, and shipments from, the Persian Gulf can recover (my base case is to 40-50% of their pre-war levels by December, 2026) we are looking into a cumulative loss of 2-3 billion barrels by year end. Even if inventory releases make up for a billion barrels that were not produced this year, we are still about to lose 3-6% of world crude oil supply on an annual average for 2026.

Knowing how tight the connection is between transportation, manufacturing, mining, construction, agricultural output and oil consumption is, that means we are facing a similar decline in real economic output, too. There is no other way around it: once inventories fall below critical levels and real world shortages begin, governments will be forced to curtail or ration fuel use—first and foremost in the industrial, mining and construction sector, and mostly in highly exposed Asian countries. Food production and transportation will be prioritized. That, however, doesn’t automatically imply that services (education, healthcare, banking, insurance, finance etc., making up two thirds of world GDP) will suffer a similar fate. In fact, we can expect a massive profit increase in these sectors, as insurance, telecom and many other companies will begin to charge higher and higher fees4—because, well, “inflation.” Presuming we don’t end up having a financial / banking crisis by year end—“just” a 3-6% drop in global industrial output—we could be thinking that we survived the crisis with higher inflation, some shortages and a 1-2% drop in global GDP. Just like we did in 2020.

That, however, is a dangerous misconception. Just as with COVID induced oil production shut-ins, the real world economic impact of the crisis will take many months if not a full year to arrive. And since this time agriculture will be especially hard hit with fuel, fertilizer and chemical shortages (on top of a massive El Nino added to already raging droughts and heatwaves from climate change) food prices will likely skyrocket in 2027. Humanity will likely have to face chronic food, oil, raw material and industrial product shortages for years to come, which will eventually affect services, finance and banking as well—albeit with a delay.5

A year or two into this malaise—as we have witnessed in the aftermath of the 2022 European energy crisis—we will see even more factory closures, lay-offs and deindustrialization due to stubbornly high energy and raw material prices / shortages, as well as from demand destruction. As for a cue what to expect, take a look at European industries 4 years after Russian gas has been shut off and pipelines were blown up. Electricity and gas prices in Britain and elsewhere in the EU are still 90% higher compared to other parts of the world, continuously eroding competitiveness and acting as a primary driver behind deindustrialization. I suspect a similar fate awaits many South/East Asian countries, whose economies were highly dependent on Persian Gulf oil imports. What we have seen so far is thus but a prelude to a much bigger and longer crisis to come. The closure of Hormuz—no matter how it ends—will cast a long shadow over the world economy.

Strategic implications

Last week I reiterated and expanded on an argument from Simon Watkins, saying that the aim of the United States as part of its ‘Energy Dominance’ agenda is to control the majority of world oil trade, in order to maintain its global primacy—even if it comes at the cost of permanently shutting in production in some parts of the world and destroying infrastructure in other places. Hence the CIA directed drone attacks on Russian refineries, prompting Russia—the third largest producer of crude oil in the world—to import gasoline. And hence the attempted, then miserably failed regime change attempt in Iran, with stopping Iran’s alleged nuclear weapons development program being used as a diplomatic cover. See, had Operation Epic Fury turn out be a roaring success—as the abduction of the Venezuelan president had earlier—the entire Middle East would’ve eventually fallen under US/Israeli rule. The Twin Pillar policy, promoting Iran and Saudi Arabia as local guardians of US interests in the Persian Gulf region, would have been finally resurrected 47 years after the shah’s western backed dictatorship was overthrown. Now that plan A (regime change), then plan B (bombing Iran) have both failed, plan C is literally on the table: turning the conflict into a semi-frozen, long drawn out hostility between Iran and the US—just below the threshold of an all out shooting war. Expect mountains of horse trading, and then a return to hostilities if talks fail, or when the US feels it has weakened Iran sufficiently enough that it can give plan A another try (maybe in a year’s time).

But what is there for the US to win with its Energy Dominance agenda? It’s fracked shale oil is not nearly as good as Middle Eastern grades, which in turn are a whole lot more suitable to make diesel and jet fuel from… The US simply can’t replace those lost barrels in any shape or form, now can it? Of course not (read this for more detail), but it can still make a huge windfall profit by selling its Strategic Petroleum Reserves to Asia and Europe. Once the SPR starts to run low, and as diesel and lubricant shortages begin to bite, though, the US will likely have to do more to accommodate Iranian demands / find alternative routes—so more Gulf oil could reach the market.67 Not too much, though, just barely enough to prevent a financial / economic meltdown… In this situation, no matter how bad it will be for the rest of the world and the global economy as a whole, neither the States, nor Iran will have the incentive to fully reopen the Strait. Both will likely want to use it as leverage: Iran over the US, the US over China (and other Asian economies).

But wait, there is much more to the story than oil. America has a surplus of liquefied natural gas (LNG) and natural gas liquids (NGL) to sell—which it can now push on to Taiwan, among many other countries in East Asia and India, at a premium price. And, as an added bonus, thus becoming the largest supplier of these fuels—used in power plants and for cooking respectively—Washington gains direct leverage over these countries, just as it did over Europe after becoming its largest LNG vendor.8 Remember, nothing happens in this Universe without energy. Energy directly translates into political power and becoming “the world’s leading energy producer and exporter” by starting and funding wars, blowing up pipelines and refineries, imposing sanctions etc. is nothing but a pure market and power grab. Just take a look at this headline of and excerpt from a recent article on the topic:

The Hormuz Crisis Has Forced India to Rethink Its Energy Strategy

Despite higher prices, India is set to import the biggest ever volumes of liquefied petroleum gas (LPG) from the United States in June as it seeks to replace still-constrained supply from the Middle East. India is estimated to receive between 1.1 million and 1.2 million tons of America’s LPG this month…

Or this one:

Taiwan’s April LNG imports boosted by US volumes

Taiwan’s monthly imports of liquefied natural gas (LNG) rose in April as US volumes surged compared to the same month last year, replacing Qatari supplies, according to customs data.

Or how about this:

European LNG Tracker

Europe more than tripled its imports of US LNG from 2021 to 2025. Given the ongoing disruptions to Qatari exports, IEEFA forecasts that Europe will source two-thirds of its LNG imports from the US in 2026.

Will this US policy and power grab lead to higher prices and more deindustrialization across the world then? You bet. But when America desperately tries to re-shore industries, making Asian manufacturing more expensive (if not putting them into an outright impossible situation) will act as a strong incentive to move manufacturing back into the States. Is this a smart, well-thought-out or morally sound plan? Of course not. Will it even work? Most likely not: America no longer has the human and infrastructure resources necessary to become a manufacturing hub—not that their citizens would be willing to work in factories, either. This policy also comes at the cost of turning the entire world against America, and with the very real risk of plunging the global economy into recession—if not into an outright depression. An event, which could eventually drag the United States, too, into the Abyss. This American power grab, dubbed as Energy Dominance, is therefore more of a sign of sheer desperation and shortsightedness—motivated by selfish interests and pushed forward in an administration which has completely severed its ties with reality—than a coherent plan. In other words it’s madness…. Well, as the famous proverb goes (and this is equally true to institutions, not just individuals):

“Whom the gods would destroy, they first make mad."

Death of the Megamachine

China is not the enemy, nor is the United States. The real enemy to confront here is an economy built on infinite growth driven by Wetiko—a psychosis devouring not only the living world but its own subjects as well. Extracting then burning ever more coal oil and gas, or mining, refining and smelting more and more metals to build electric devices cannot continue for much too long due to a lack of adequately high quality, easy-to-get reserves (which makes the whole endeavor profitable). And it really doesn’t matter if we call them petrostates or electrostates—both models are equally and totally unsustainable. The evidence has been laid bare for the whole world to see. All bursts of growth eventually end, then give way to desperation as decline threatens to set in.

The bad news is: this decline cannot be stopped—only hastened—as it is driven by not political or individual decisions, but the logic of a complex system with all its economic and cultural incentives built on the fastest possible draw-down of non-renewable resources. This civilization is rapidly passing its sell-by date, and faces a long tumultuous decline—and neither trying to build an electrified surveillance utopia, nor reinstating oneself as the petro-king of the world can change that. The good news is, on the other hand, that there is a way to restore what has been broken; if not fully, then at least to a degree where subsequent generations—of not just humans but all living beings—can live a materially poorer but certainly more fulfilling life. In order for us to live, the Megamachine must die.

Helping nature to regenerate is the only way through our predicament, using whatever resources we may still have to repair the damage we have done to Nature and to wean agriculture off of fossil fuels, chemicals and of their many other disastrous practices. This doesn’t meant that we have to rush back to the caves, nor that we must hide in a bunker. Mineral resources will not run out from one year to the next plunging the world into chaos. It means seeking ways to live a more fulfilling way of life, one not centered around chasing profits and limitless growth, but one which is aimed at finding the balance between what’s still possible and what needs to be done to ensure a peaceful transition into a future of less consumption and more connection. Actively trying to hurt others for our way of life to continue just a little longer will certainly not get us there.

Until next time,

B

Thank you for reading The Honest Sorcerer. If you value this article or any others please share and consider a subscription, or perhaps buying a virtual coffee. At the same time allow me to express my eternal gratitude to those who already support my work — without you this site could not exist.

As the famous quote from Upton Sinclair goes: “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Economists, traders, politicians and even industry insiders will never admit that we face global limits on resource extraction, as saying so would imply that all their investments and advice (based on the assumption of growth going on forever) will eventually turn out to be worthless. Their livelihood literally depends on maintaining a belief in infinite growth.

What looks to be sure for the time being, is that conventional on-shore and shallow water crude oil extraction has peaked around 2004, then continued to decline ever since as depletion kept accelerating. Their replacement with unconventional and deep sea oil (together with adding natural gas liquids, which are anything but oil) has managed to keep up a semblance of growth, but even these new sources have their inherent limitations, beyond costing much more energy to get than conventional supplies.

Power plants cannot operate beyond their physical limitations: heat, sunlight, wind or hydrological power cannot be converted into electricity at a 1:1 rate. Usually it’s around 1:3 (for every kilowatt of electric power produced you need 3 kilowatts of heat input when it comes to fossil fuels). At best you can get 1:2 in case of wind turbines and combined cycle gas power plants, or as low as 1:5 in case of solar panels. If you also take weather into account—you know the Sun doesn’t always shine—you need to capture 5 to 50 times as much wind and sunlight than what you actually need, convert it into electricity than store the excess for later use. And then we haven’t even mentioned losses during transmission and storage… This means electric systems must be brutally overbuilt using non-renewable materials, then this exercise must be repeated every 1-2 decades or so as old equipment fails then needs to be replaced. The math simply doesn’t work: neither in China, nor in the United Arab Emirates, one of the sunniest places on Earth.

Consider also that while logistics firms are directly hit with an increase in fuel prices, many other service companies (law firms, banks, insurance companies, financial intermediaries, educational institutions do not pay for their fuel, their employees do). Unless, however, their services are absolutely essential / mandatory to use, customers might still turn away as they face higher cost of living, eventually leading to many service companies to go bust.

If we accept the premise that at least some of the financial elite knows how dire the real, material growth prospects of the world is, then they have to choose between two options: wait for the system to collapse under the weight of its internal contradictions or to engineer a crisis where they preposition themselves to buy assets on the cheap, then restart the system under a different currency regime (CBDC-s, anyone?). The massive US data center build-out can be thus interpreted as America prearranging itself to take the lead in a new, tokenized, surveillance based financial system, where big tech, military tech and banks merge into one big blob. I can but hope that I’m proven wrong.

Think of the coming Middle East pipeline boom not as a solution, but as a deal sweetener, as not nearly enough capacity is being planned (let alone built) to circumvent the Hormuz-blockade. Rather, it’s an incentive to keep some players (Iraq, Syria, Turkey) on board, then exert control over them (and Europe) through pipeline ownership rights and fees. “The Four Seas Initiative would deliver four compounding strategic goods: European energy sovereignty from Russian and Iranian dependence; American commercial primacy in the Middle East’s most strategically leveraged infrastructure; Syrian economic reconstruction underwritten by transit revenues; and a durable geopolitical settlement that rewards alignment with the West.” Put in plain English: these pipelines would serve to maintain Western hegemony, not healthy supplies.

While the number of ships leaving the Gulf (mostly through Omani waters) has hit a new record high since the start of the war, there are still remarkably few ships entering the Gulf. This means, that traffic will once again subside as soon as all hitherto trapped ships—carrying 60-100 million barrels of oil and petroleum products—leave the area. For your reference: this is 3-5 days worth of traffic in pre-war terms, not a game changer in any way.

Poor Europeans thought that switching to “renewables” on a continent which regularly plunges into months of dark, windless, cloudy weather (known as winter elsewhere but here mostly without snow) would somehow save them… Gas was sold to their public as a bridge fuel to “renewables”, but in fact it were “renewables” which ended up becoming the bridge fuel for more gas—American LNG to be precise. At least while US gas reserves last, or domestic demand from data centers render exports uneconomic / impossible… Leaving Europe with a gaping energy hole.

I always appreciate these overview entries.

The thing that keeps hitting me is..... we can still have 80% of our technological society, at 20% of the cost. Small 3D printed homes (perhaps shaped like beehives), with 2 PSI water systems, and 12 Volt electrical. A little woodstove for hot water, and a cooking top. The TV could run from an inverter. That sort of thing.

Cars (1/10th the weight of what we commonly have now) could be electric, limited to 35 kph and 50km range... (but easily rechargeable from solar panels) ... perhaps built like Sinclair (ZX 81) suggested. Slow enough that it could self drive (or generally follow a metallic painted line), and not be too dangerous to others.

We have the wireless internet for work and entertainment which should be reasonably inexpensive to maintain... especially it it slows down a bit. Why are we not building a step down solution which anticipates a lower energy future?

In Canada, it is no longer possible to build a modern home for the price of conforming to regulations. That right there screams.... its time to try new things. Everything could be so much more enjoyable... with locally fabricated as much as possible... things. Almost everything substantial could be fabricated with 3D Printers, C&C laser metal cutters, and repurposed components provided by the last 50 years or so.

Perhaps a 25 hour work week would become the norm, so that more time could be spent throwing a ball around, and learning localism skills (building, gardening, beer etc).

B says: "This American power grab, dubbed as Energy Dominance, is therefore more of a sign of sheer desperation and shortsightedness—motivated by selfish interests and pushed forward in an administration which has completely severed its ties with reality—than a coherent plan. In other words it’s madness."

This is what Emmanuel Todd called American Nihilism. He is absolutely correct. But don't forget Israeli Nihilism. Together, these two forces doom ALL those invested in the System. Detach as much as you can.